It was a dreary day, and I was catching up over coffee with a friend of mine whom I hadn’t seen in a couple of years. And we were talking about startups and fundraising. This friend has known me since when I had my company LaunchBit, and she knew just how much I hated fundraising back in the day. In fact, when I was running LaunchBit, the fundraising process was super tough for me. In fact, it took a huge toll on my health.

Back in 2011…

“We can’t find anything wrong.” said the physician.

There I was at Massachusetts General Hospital. I had been referred to a specialist to check out a problem I was having. My problem was tough to explain – I kept feeling like someone was constantly poking me all the time with a pin. Just everywhere all over my body. The prickly feeling didn’t stop anytime during the day – even when I was trying to sleep. It had started a few weeks before and it just would not go away.

After seeing a number of physicians who could not figure out what was wrong, Massachusetts General Hospital was the final stop. MGH was a world premier hospital with a billion and one specialists and researchers including in fields such as the nervous system. All these doctors appointments were a bit of a distraction for me, because I was in the middle of raising a seed round for LaunchBit. But this issue was becoming so bad that I couldn’t even sleep.

Fundraising had been a stressful process, and I had felt so much pressure to raise a $1m round. And, after raising almost $400,000, I decided to just stop. I wasn’t getting any more momentum on the round, and my health problems were really starting to bother me. Immediately after halting my fundraising activities, surprise surprise, all of my ailments stopped and magically disappeared. There was never any scientific explanation or diagnosis for what had happened. The only explanation that I have for myself is that I was just so stressed that weird things were happening to me because fundraising was taking a toll on my health. Fundraising was definitely not fun to me back then.

Back to the meeting with my friend. “So why do you like fundraising so much now?” she asked.

“Hmm…that’s a good question. Because I now understand how to do it. And, because I’m good at it – hah!” I responded half laughing.

It was even hard for me to believe that I could get good at fundraising.

In the past 7 years, I’ve learned so much about fundraising – partly from my own fundraising experiences LaunchBit, but much more so through helping hundreds of founders I’ve backed over the years with their raises and in raising Fund 1 for Hustle Fund.

7 years ago, I didn’t understand how to fundraise. I think when we hear the word “pitch”, it almost seems to imply that we are talking at someone. But fundraising could not be further from that.

My biggest learning around fundraising is that fundraising is actually a series of dialogues – not pitches – and success is contingent upon need finding and finding the right investor match.

The reason I think fundraising is so fun now is that I’ve learned that fundraising is more of a customer development exercise out of the Lean Startup playbook than anything else. And that’s fun.

A noob fundraiser will go into a first meeting, open up his/her deck, and start going through the slides. In doing so, you don’t really know how your story is landing. You’re not having a conversation. But, an experienced fundraiser knows that the goal in going into your first fundraising meeting is to ask lots of questions and walk away understanding what next steps make sense. You should understand your potential investor’s pain points. Is there something you can solve for a potential investor by having him/her invest in your company? Do you have a solution for those pain points?

There are many reasons to invest

For example, let’s say we’re selling pet food – hippo pet food – and let’s say that I were raising money for this company.

There are a number of reasons why someone might like to invest in this company. It could be that an investor wants:

To make a lot of money and believes that hippo pet food is an amazing market

To invest in a basket of e-commerce companies

To invest, because he/she believes in me personally

To invest in more female entrepreneurs

To invest, because he/she has a pet hippo and really loves the product

To invest, because he/she believes that I have a strong network and wants to get tapped into it

To invest in a bucket of Xooglers’ (ex-Googlers) companies

The list goes on and on. As you can, there are many reasons why an investor might like to invest in this business. And my job is to ask lots of questions in a first meeting to learn what an investors’ interests and challenges are. And can I figure out which of these reasons, perhaps, might be one that resonates with a potential investor.

I think we fixate too much on what VCs are looking for, but it’s important to note that the world is filled with many would be investors, including individuals, corporates, and family offices.

In general, most VCs are trying to maximize their dollar return in the shortest amount of time possible. (This is reason #1) But, for an angel investor, there are many other reasons to invest, and some of those reasons may be #2 or #3 or #5 etc…

Fundraising is about doing customer development

It is your job as an entrepreneur to figure out what a potential investor is interested in in a first meeting. Can you help that person or that company achieve its goal. If the investor is trying to invest in more e-commerce companies, you’ll want to tailor your story to that thesis, and if the investor is trying to invest in more women, you may want to play up that angle.

Your job in the first meeting with a potential investor is to ask a lot of questions – ala customer development style – to understand how you might be able to tie your story to their problems and interests. And so your pitch should not be stagnant, and although you may have created a deck before the meeting, it’s important to tie your talking points together as a solution to the problems you learn about in that meeting.

The first meeting with an investor is really about truly understanding their needs and triaging whether you think your company might be a good fit for that investor. Your job is not to try to convince a potential investor to invest. Your job is just to triage. It is much easier for you to close an investor who is already bought into your story than it is to try to sell an investor who is not bought in. And it’s ok if someone is not a good fit. In fact, I would just address that head on — “It sounds like this might not be a good match — you’re generally a series A investor and you’re looking for a lot more traction. Why don’t I put you on my newsletter, and perhaps there may be a fit down the road?” Addressing things clearly and directly is the best way to communicate with investors, and it’s ok if there’s no match.

There are billions of investors

I’ve observed over the years that when founders create their list of investors they want to pitch to, they often draw from common directories. Such as Crunchbase. Or AngelList. Or various Excel spreadsheets that are passed around. It’s often the same set of hundreds of funds and about 100 angels. These lists are a great place to start for sure. But what I’ve found is that these lists also narrow people’s thinking. Why do founders just pitch these people? Why not the billions of other people in the world? There are so many rich people or even people who are not rich but may have conviction to write a small check. By limiting ourselves to these lists, we create unnecessary pressure on ourselves. You end up in a weird mindset — if I cannot convince these people to invest, I’m hosed. Right? A bit of an exaggeration, but has anyone else had that mindset before? I certainly have.

But this is the wrong way to think about things. The right way to think about fundraising is with a growth mindset. There are billions of people in the world – many of whom are rich – any of these people could potentially invest. This takes the pressure off right away. The game changes from “How can I convince this small group of people to invest in my company” to “How do I triage people quickly and get to meet with a lot of people quickly?”

Once you have that mindset, then it’s just a matter of finding potential investors to have a conversation with, figuring out quickly whether they are a good fit, and if they’re not, move on quickly. Instead of wasting time trying to convince someone to invest, you want to actually spend as little time with people who are not a good match to focus your energy on getting new meetings. Your job is not to try to pitch at people or convince. Your job is just to have a conversation and do need finding, triage accordingly, and then rinse and repeat. (See my post on finding potential investors.) That is what fundraising is all about when done right.

For people who are not a good fit, you definitely want to cultivate those relationships. Put all of these people on a monthly newsletter with your clear progress. Much like in B2B sales, if a lead is not a warm lead, you should use automation to keep those people engaged but don’t spend a lot of time with them until they are actually interested.

When I was fundraising for my startup many years ago, I took the totally wrong approach. And you can see that by limiting yourself to some silly list that you have and putting pressure on yourself, fundraising can be a bear. But if you can change your mindset and approach, it’s actually pretty fun.

Today’s blog post is all about the annoying things that VCs commonly say or ask. I did a call out on Twitter this week and these are the VCisms that the crowds have bubbled up as the most annoying things out of a VC’s mouth.

This one was cited a LOT by many people on Twitter in various forms! There were variations — e.g. substitute Google with Amazon or Facebook or any other big company.

Admittedly it’s a valid question — what if the 800 lb gorilla in your space does copy you? What is your edge? How will you win?

Here are a couple of answers that may help:

A. Large companies are so large, they aren’t able to prioritize or even care about your “small” opportunity relative to their huge company. In the case of Google specifically, it has actually been shown that building a Google product competitor can actually be a great opportunity. Many people would much prefer to pay for products so that they can get customer support when something goes wrong — a free Google product will never a customer’s calls or emails.

Companies like Mixpanel, Optimizely, Superhuman, and many more have built big businesses by going head-to-head with a free Google product by charging customers and providing a better experience.

So it’s actually validation of your market if Google is interested in your space.

B. Big companies, by definition, are no longer nimble. You, in contrast, are able to run circles around them. Can you prove that you’re nimble by shipping quickly? Can you show that customers love you more than Google? These are concrete things that you can point to in your conversations with VCs.

2) We don’t invest in hardware (only to find out that they led a round for hardware) (@peterjcolbert)

This is an interesting one, because you see VCs deviate from their thesis sometimes. (Every VC does it – we’ve done it too.). VCs will often say they don’t invest in hardware. Or ad revenue based models. Or e-commerce. Or in some geography. And then you see a portfolio company on their website that is clearly in one of these categories.

You should just ask a VC about it directly.

The reason for this is usually along one of these lines:

A. They used to invest in that category but are now over-indexed. Or they invested in that category previously as an angel or with a past fund. I.e. they used to make those investments but no longer do.

This is important to understand, because if the reason the firm is passing is that they are waiting for some liquidity on existing positions in your space, there could potentially still be an opening for an investment later. This is rare, BUT possible – this has happened once to a company that I’ve backed before.

B. They are experimenting outside their thesis. E.g. They may not usually invest in South America, but they may make 1 investment to learn about the market. They may not invest in hardware, but may invest in 2 companies to learn about the space.

Unfortunately, if this is the case, you can try to hard to convince a VC to do more experimentation in that category, but because VCs have mandates — i.e. they have an agreement with their investors that they would focus on investing in certain categories / theses, they will likely not want to deviate *too* much from their thesis. VCs are judged by their investors on whether they end up investing based on the strategy that they claimed they would.

C. They had a special relationship with the founder.

There is nothing you can do about this. People back their friends all the time regardless of what they are building.

I think it’s easy to walk away fuming mad thinking that a firm is filled with hypocrites, but it’s worth just bringing up with a VC: “Hey you mentioned that you don’t do hardware, but I noticed on your website that you’ve invested in X. Am curious how that fits your thesis?” You may not like the response and it may not change anything, but on rare occasion it may open a door for you.

3) I don’t think this can be a venture scale business. (@kirbywinfield)

I’m of two minds on this one.

A. There are a lot of companies who seek out venture funding who are actually NOT a good fit for VC investors. Entrepreneurs should be aware of the return profile that VCs are looking for. Loosely speaking, VCs are looking for a minimum of 100x return in the course of 5 years or so. This comes out to achieving roughly $100m runrate within the next 5 years. Is this what you want to do?

B. However, on the flip side, what ideas will be able to achieve $100m runrate in 5 years is tough to say. VCs often have preconceived notions above what can get to this level and what cannot — and they are often wrong. Companies that tend to get overlooked are in categories such as e-commerce, for example. Are you selling a widget that will likely max out at $5m in sales per year? Or are you the next Stitch Fix?

My advice here would be to first understand for yourself if you want to be growing a business that goes to $100m in annual revenue in 5 years (and the work / hiring that will be required to do so). And if so, what do you think that path looks like if everything goes well? How will you get to $2m runrate this year and then more than double your sales each year thereafter?

And if the answer is that you don’t want to run this type of business, there are other avenues of funding. Angel funding, crowdfunding, revenue-based financing are all good channels that are now rapidly growing.

4) But how will you manage being a mom AND running a startup? (@hustlefundvc)

Ugh. Are we in the 21st century? Move on from any VC who asks this. It’s not worth it.

5) We’d be interested when we see a bit more traction. (@msuster)

Ah, the classic ask for more traction. Basically, the VC doesn’t have conviction right now, but maybe, just maybe, more traction would give him/her the conviction to do your deal. The reality is that most investors can’t articulate what level of traction they would want to see in order to invest. Obviously, if you earn $100m in the next 2 months, everyone will be onboard, but what if you get to $100k / mo runrate in the next year — is that interesting? Well…it depends. And unless you are an asshole or a fraudster, VCs always want to preserve optionality to see you in a year and check on your business.

So, although this is a frustrating response, the right way to play this is to triage investors quickly. Put this VC in a “not interested” bucket. Continue to send him/your monthly investor updates, but you’re better off trying to find someone who has conviction today than trying to convince someone to get conviction — even with traction. You just need to meet a lot of investors and triage a lot of investors quickly in order to find the right investors to bring into your company.

6) Maybe you should raise more and grow quicker. (@justinpushas)

This is just a stupid comment. If a VC really believes in your business, he/she will commit to your round, and will either help you fill your larger round or write a bigger check. But, investors who say things like this without any action are either just oblivious or not helpful, and should just move on from these investors. As we all know, founders who struggle to raise $250k are also going to have a tough time raising $2.5m.

That being said, I would recommend that every founder develop multiple fundraising plans. This will allow you to pitch a different amount of money to bigger or smaller investors with different milestones and goals that you would achieve with different investment sizes. And then if you do receive this question, you can point to a larger fundraising plan and mention that you have thought about a larger plan and are open to raising more money but are also not limited in growth if you cannot raise that amount now.

The herd of sheep comment! A variation on this is, “I’m committed once you have a lead.” This is a positive way for a VC to say no for now, but if you have enough fundraising traction, then he/she wants to get his/her foot in the door.

It’s important to clarify what a VC means by this, though. Does this mean he/she is interested:

When you have most of your round committed?

Once terms have been set?

If another investor is taking a board seat and is providing “serious responsibility ” for the investment. (i.e. no party rounds)?

This is important to clarify, because VCs mean different things when they ask about a lead VC.

If it’s the former — come back when most of the round is committed — you can build your round in many different ways. You can bring together a party round of smaller investors without a lead on a convertible note or SAFE. It’s actually quite common these days for a smaller fund to set terms on a note or a SAFE and bring together a round that way.

And if a VC is just looking to evaluate terms, then you can create your own terms on a note or a SAFE and present those to the VC.

And lastly, if the VC is looking for a true “lead VC” to invest the majority of the round and take a board seat, etc, then this is a completely different ask from the prior two.

8) Let me know how I can help! Founder asks for help. *crickets* (@quan)

When I started my VC career, I asked this question to a few entrepreneurs I met with. I genuinely wanted to be helpful. Then I quickly realized that there was literally nothing I could help with. Hah. Every founder just wanted investment dollars, and if I weren’t investing, I couldn’t even do introductions to other investors, because it would be a bad signal.

10) Contact us if you like but we prefer warm introductions. (@cwlucas)

I find this ironic — VCs prefer warm introductions, and YET, there are a lot of VC analysts who send outbound emails to startups completely cold asking to chat!

My recommendation here is to try to get a warm referral to a VC. Just in general, it’s always better to have a common connection to build rapport with. That being said, a lot of the newer VCs (esp microVCs) are ok with cold emails. (For reference, 20% of our deals come in completely cold, and we see no difference in performance between the cohort of companies that came in cold vs warm)

My prediction in the next 5 years is that the VC world will move to largely accepting *good* cold emails. Most cold emails are terrible and will likely be ignored, but you do have a shot if you can send a strong cold email.

11) (Live product, thousands of users) “Yes but what *traction* do you have?”

(Gets in to YC) “Your valuation is so HIGH now!” (@kristentyrrell)

This is the typical Goldilocks and the 3 Bears problem. At first, you’re “too early” — you don’t have enough traction. And then, once you get there or another investor participates in your round and drives the valuation up, then you become “too late” — the valuation is too high.

As frustrating as this is, this is just a matter of luck / timing and fit. As pre-seed investors, I am susceptible to this as well in some sense. We invest really early (from a valuation perspective), so, by definition, we are not looking for traction. This means that we make our decisions entirely based on gut instinct of the opportunity. So, if we don’t have conviction in the business idea, we will pass. And once a founder proves with traction that we were wrong, we still won’t be able to invest, because the valuation will be too high. That’s frustrating but I’d say frustrating for VCs who miss out too — as you may have seen from the Uber IPO, lots of VCs lost out on a lot of money, because they didn’t have conviction in the idea.

There’s a lot of gut instinct in this business, and to be honest, to be great at it, you only need to be right about 20-30% of the time. It’s like baseball – you strike out most of the time. If you were to work at any other job — imagine if you were say a surgeon — if you were right only 20-30% of the time, you would be fired and everyone would be dead.

Now, this doesn’t apply to multi-stage investors. If they miss out on your seed round, you can still re-approach them at the series A or the series B.

12) Why hasn’t this been done before? (@jacobshiach)

This is a seemingly ridiculous question, and it may also seem that a lazy VC may not want to do his/her own homework. But, this question is meant to test how you think through trends and changes in your ecosystem. If you believe that markets are efficient, your opportunity should not exist. Why? Because if it’s an obvious opportunity, it means that everyone would have done it already.

So what is your key insight or secret that enables you to know about this opportunity that others do not. Is it your domain knowledge? Is it that the opportunity is in between two sectors that most people are not familiar with? Is it a behavioral trend that is happening to a certain demographic that you are a part of but most entrepreneurs are not? Whatever it is, every startup needs to have a good answer for this. Heck, even funds get asked this question — why aren’t other funds doing your strategy? And I’d say, as annoying as it is, it’s a legit question.

13) How can this be a billion dollar company? (@rkorny)

You might wonder why VCs are so obsessed with billion dollar businesses. This is because the economics of running a fund are so tough. Basically, you have a bunch of portfolio companies that will completely fail. So whatever 1-2 winners you have, will need to make up for that failure plus much more to return multiples for the fund. (Read more here: https://elizabethyin839669270.wordpress.com/2016/05/15/whats-the-difference-between-angels-and-seed-vcs/)

This means that VCs are looking for 100x+ multiple at a minimum on a successful company, and if they are coming into your round at the seed stage — say at $10m post money valuation, 100x on that is roughly a $1b exit not accounting for dilution. So this comes back to the question from above — do you want to be raising money from VCs? Is this the type of business you want to be running?

14) What’s the moat? (for a seed stage company) (@chloealpert)

This is super annoying for a seed stage company, because obviously there is no moat.

Thinking longer term, however, simplistically, there’s only one way to have a moat — and that is, your customers love you so much, they will never want to leave you and keep coming back. There could be a lot of ways to build this — e.g. you have a better user experience / product, you have more data to make your solution better / more accurate, you have greater network effects and therefore have a better product, etc. Depending on your idea, the way that you achieve this outcome will differ a lot.

VCs want to understand at scale, how you will achieve this. This is especially key for companies that have commodity products — such as finance. You don’t want to be competing on price or better deals, etc. How will you build that better / smarter product? How will you build that retention in business model? VCs want to understand how you think about this 5 years from now more than what things look like today.

15) We’re going to pass but will be cheering for you from the sidelines. (@comaddox)

This is just a ridiculous phrase and pet peeve of mine. What is this? Bring It On?

Last week I gave a talk about wealth to students, and I thought that it would be worthwhile to share this here on my blog.

I’ve learned a lot about building wealth over the past 20 years (though am not wealthy yet!). But, most of my learnings on wealth have come from observation of the people around me in just the last 5 years or so.

First off, I know that many people don’t care too much about money. And that’s fine! Many people have very noble missions in life. But — wealth gives you power — the power to change things. To have influence. To put towards good causes. Whatever you want.

I’ve met so many people over the years who have said to me, “I don’t care about becoming rich – wealth doesn’t motivate me. What motivates me is ABC cause”. And that may be true, but you need wealth to drive the things that do motivate you to really have an impact.

So, let’s talk about the general strategy to becoming wealthy. I think there are three stages:

Saving money

Investing in low-risk / low-return assets

Investing in high-risk / high-return assets

Let’s dive into each of these stages.

Saving money

The first stage, I think, is obvious to many people. When you don’t have any or much money, the best way to get started in building wealth is to save money. Some people are good at this. Other people are not good at this. And people have different strategies on how to save money. For example, my mom came to this country with just $25. She and my grandparents were incredibly thrifty people. One thing that both of my grandparents did was to have all their teeth extracted when they moved to America in order to reduce their dental expenses! Other people have other strategies for amassing cash savings. Some people get the highest paying job that they can. Other people don’t eat avocado toast. I think we all have different methods but in general, I think everyone understands that saving money is important in the very beginning.

Investing in low-risk / low-return assets

The next stage of building wealth is about taking whatever savings you have and putting it into low-risk and low-returning assets. Because after all, you can’t really afford to lose your newly earned cash because you don’t have a lot of cushion.

Surprisingly, we don’t really learn anything in school about investing, which is an utter shame. Most people end up learning a little bit about investing from what they read online or places like Money magazine. Super low-risk and low-returning assets include things like government bonds, savings accounts, and even CDs. For the most part, you won’t lose your money in these assets, but you won’t make any money either.

A medium-risk / medium-return asset class that a lot of people know about are index funds — these are baskets of shares of public stocks. Historically, index funds have returned about 2x over the course of a decade. In other words, if you put in $100 into the S&P 500, 10 years later, you might have about $200. There is a lot of variation, however, in the returns depending on the year. For example, in 2018 alone, a typical index fund returned 20%. In other words, if you put $100 into an index fund in January 2018, by December, it was worth $120. On the flip side, index funds also take a dive in value during recessions. In 2008/2009, the value of stocks dropped about 50% almost over night! I call index funds medium-risk / medium-return asset classes, because unless the entire economy goes belly-up and the world ends, your money will likely not go completely to zero in the long run, because index funds are betting on the overall macro economy doing well. And if that isn’t happening in the long run in the world, then we probably have much bigger problems on our hands — i.e. the world ending / we’re all going to die.

Investing in high-risk / high-return assets

I think the asset class that is talked about the least are the high-risk and high-return assets. There are a lot of these kinds of assets. What I didn’t realize until my 30s was that the wealthiest people make their money on investments — these kinds of investments. They don’t make money on their salary. They don’t make money on their index funds. This is something that most of mainstream America does not realize.

There are many different types of high-risk / high-return assets, but what I want to focus on for this talk is the startup investment asset class. There are many ways to invest in startups. At the most hands-on level, you can build your own startup — invest your own time & money into your own company. You can work for someone else’s startup or advise someone else’s startup. You can invest directly into startups with just money. You can invest in funds that invest in startups. And at the most hands-off level, you can invest in funds that invest in funds that invest in startups. All of these are risky — i.e. you may not see any return on your time or money at all. Or, you can see a tremendous return.

I think many people think that to invest money into startups (whether directly or into a fund), you need to be super wealthy and as a result, they haven’t really thought about investing into this asset class. For example, many years ago, a friend of mine was raising money for his fund. He told me at a very high level about his new fund and wanted to understand my interest in learning more and potentially investing. I immediately dismissed the idea. I didn’t even look into the opportunity, and I don’t even know what his strategy or thesis was. This is because I believed I wasn’t wealthy enough to participate in such a high-risk, high-return asset class. I felt that I hadn’t accumulated enough cash to do this. Years later though, when I was raising money for Hustle Fund 1, I thought back on that memory and I realized that I had been wrong to immediately dismiss the opportunity. It occurred to me that even though I don’t have a lot of wealth, there is always some amount that makes sense to participate with in a high-risk and high-return asset class.

For example, let’s say that hypothetically you have saved $100,000. And let’s say that you know you will not need to touch $25k of that money until after you retire but it’s not important to your retirement savings either. In other words, you can afford to take quite a bit of risk with some subset of that $25k. If you lost it all, that wouldn’t be fun, BUT is there an amount that you’d be willing to potentially lose entirely — to risk potentially achieving a 100x multiple on that investment? E.g. would you be willing to risk $5K? The likelihood of that $5k investment might go to zero but if in the off-chance it did well, it would turn into $500k. This is not some weird hypothetical. As a concrete example, Uber has been in the news for their IPO. A $5,000 investment into Uber at the seed stage would be worth $25M today! That’s life changing for most people, and it’s only a $5k risk.

But, I don’t think most people think about their finances from a portfolio construction perspective. I think most people fixate on saving money first and then *maybe* they buy a house or invest in index funds. Most people never think about investing in high-risk / high-reward asset classes. And these are the investments that are life changing and make people really wealthy. Just to be clear, when I say “these”, I’m talking about high-risk / high-return assets, not necessarily angel investing, and there are all kinds of high-risk / high-return assets.

Determining how much money to invest in a high-risk / high return asset class such as startups is really a matter of portfolio construction. You would never want to risk all of your savings in this asset class. But there is some percentage that makes sense. Maybe it’s just $1k. Maybe it’s $5k. Maybe it’s $25k. Maybe it’s nothing right now but in 10 years, it could be $5k. But most people just never think about this.

This brings me to my next point. I think a lot of people think that angel investors deploy a lot of capital into startups. Ten years ago, I used to think that angel investors typically invested $25k-$100k into each startup. There are certainly angels at this level. But what I’ve come to learn over the years that most people don’t talk about is that there are actually a LOT of angels who only deploy $1k or $5k or $10k into each company. And if you think about it from that perspective, for most professionals, putting in $1K or $5K is actually not that big of a deal. Your bonus each year might cover your startup investing without needing to specifically save for investing in high risk / high return asset classes.

People ask me, “who are these startups who take $5k investments?” It’s simple – most founders. But, you have to earn it. You have to be:

A fast decision maker — you are not putting in a lot of money, so your due diligence process has to be less than an investor with a larger check

Not annoying / not a pain in the butt

Value add – there are lots of ways to be value-add even if you are not in the same industry nor know anything about startups; here are ways that anyone can help a company:

Provide feedback on a pitch deck

Provide feedback as a consumer on a user experience

Do introductions to other investors or potential hires

In fact, what most people don’t realize is that it’s generally easier to get into early stage fundraising rounds with just a small investment check. If the round is oversubscribed, founders will consider adding a $5k investor if they think the person is worth it. It’s just an extra $5k of dilution. No big deal. If you were investing $200k and the round is oversubscribed, you likely won’t get in because founders wouldn’t want to sell too much of their company. If the round is undersubscribed, you can get into a round anyway at any amount.

Now sometimes, there are minimum thresholds for investing. For direct startup investing, this is often flexible, especially if the round is not oversubscribed. But for funds, this isn’t true. Part of the reason for this is that both startups and funds can only take on 99 accredited investors per SEC rules. This means that if a VC fund is raising $100M dollars, the average investment check for each investor has to be over $1M each. But, I wouldn’t let potential minimums deter you from looking into an opportunity whether it be startup investing or other high-risk / high-return assets.

Investments beget investments

Once you start investing in startups in some fashion, there are all kinds of other benefits. You get to mingle with other investors. These people are well-connected and can show you better deals, introduce you to other influential people, and help you out in so many ways. Many angel investors fund other angel investors’ businesses. This is partly why I know so many entrepreneurs who invest as small angels — even if they don’t have a lot of money — $1k or $5k investments here and there buy not only an investment but also a network. The act of investing itself allows you to build rapport with other investors in an easy way. And it doesn’t matter how much you’re investing. No one goes around saying how much they invested into a company. Just being an investor gives you benefits.

Rich people get richer

The last point is something that bothers me a little bit. These days, there is a lot of talk about salaries – about how women, for example, don’t get paid as much as men for the same role. And I certainly think that’s an important problem to solve. But what isn’t talked about at all, is that there are so few women investors. Making money on investments — above and beyond — makes way more money than any salary. But women are getting left behind because as a vast generalization, they don’t invest in high-risk / high-reward asset classes. If you had invested in Google at the seed round, you wouldn’t even care about working there. Investing can be life-changing as we’ve seen from the numbers above with the Uber IPO example.

When we started Hustle Fund, we pitched many of our friends, asking them to invest in our fund. It was a very eye opening experience. For many of our male friends whom we pitched, they saw Hustle Fund as a great opportunity. They saw all the upside potential of this fund and invested. When we tried to pitch female friends, almost all of them turned us down — in fact, most didn’t even want to hear the pitch! Now keep in mind, all of these people — both men and women — all worked in similar jobs and made similar amounts of money and had similar educational backgrounds. But what was fascinating is that our female friends didn’t see opportunity. They saw risk. They thought about all the things that could go wrong. They thought about losing their money. The differential between the number of male investors and female investors in our first fund is so huge that at our first LP meeting, one of my (few) female friends who invested commented “Where are all the women?”. I didn’t have a good answer.

That made me think back to when my friend offered me the opportunity to invest in his fund and I didn’t even look at it. In retrospect, I absolutely should have looked at it and heard the pitch. And if I liked it, there would have been some amount that I would have offered to invest. It may not have hit his minimum, but I should have looked into it. This is a mindset shift that I’ve had over the years and one that I strongly believe that everyone should go through regardless of gender and demographic background. For those of us who didn’t grow up in families that think in this way, it’s a hard mindshift, but one that I think is especially important for people who are not exposed to wealth.

People who do well on a high-risk / high-reward investments often take a good portion of those earnings and pour it into many more high-risk / high-reward investments, and the rich become richer. A number of my friends who started out as small $5k angels here and there have gone on to make good money and pour that back into more investing. And in just a short 10 years, they have done really well for themselves and are more than set for life. Meanwhile, I’ve observed that my other friends who don’t do any of this high-risk / high-reward investing will likely get to the same point as these angel friends of mine in about another 40-80 years. There are many different kinds of high-risk / high-reward assets, and I use startup investing as one example (that may or may not work for everyone), but I wanted to illuminate this overall asset profile (high-risk / high-return). The difference between the group of people who invest in high-risk / high-return asset classes and those who don’t isn’t intelligence. And it isn’t job function or salary. It’s specific education around investing in high-risk / high-reward asset classes. You will, of course, need to do your homework around specific opportunities in the latter and decide what makes sense, but thinking about your own portfolio management and how you bucket your money is the critical point.

So wrapping this all up, if there’s only a couple of things that you took away from this talk:

You make money from investing – not salaries. You don’t have to be a professional investor, but you should take cash from your job to invest in order to amass a lot of wealth.

Think about your own liquidity needs and start to move towards some riskier and higher reward investments as you amass more cash than you need. Everyone will have a different amount that makes sense, but this is how you should be thinking about investing.

Start early — even as early as today.

If you don’t have an investment mindset, change it — regardless of what profession you are in. Your salary doesn’t make you wealthy.

And so as you go into the world and start to look for your first job and get to that first stage of amassing wealth, think about your plan for getting to the third stage. Because amassing wealth gives you freedom and power to accomplish the mission that you actually want to tackle.

Go become wealthy and change the world! Thank you for having me!

Disclaimer: This talk / blog post is not investment advice. In case you are so inspired to run out and buy lottery tickets of any form – figuratively or literally, I encourage you to consult your financial advisor, your friends, your family, your dog and anyone else you trust on financial matters instead of relying on random blog posts such as this to make life changing decisions. Thank you.

Thank you to Stonly Baptiste for his suggestions and feedback on this post!

“Contrarian perspective here – it’s ok to *not* meet a founder in person before deciding to invest.”

This set off a tweet firestorm — mostly with people telling me in some form or fashion that I was wrong. (Side note: what I love about the VC industry is that people tend to have incredibly strong opinions based on limited or no data :) )

It’s interesting — at this point, I’ve been investing in early stage startups for almost 5 years. And, I still have a lot to learn. But I’ve also personally interviewed 1000+ early stage startup teams.

Most of these teams in person.

And after looking at all this data about interviewing, I believe that it actually doesn’t really matter *for me* whether I interview teams in-person or remotely. Let’s dissect this a bit:

First, why should you interview startup teams in person?

1) I think cultural and historical business norms would say that you should always try to meet people in person and try to build rapport in person to win a deal.

While I don’t think anyone has great proof on this, intuitively, I believe this is true. What better way to win a deal than to fly to a founder and just show up and say, “Hey, I want to invest”.

So for investors playing in highly competitive spaces, this makes a ton of sense. E.g. investors going after a hot series B deal. Or for investors chasing after founders who came from Facebook and MIT who are building the next scooter company that utilizes AI. Building rapport is really important to winning hot deals.

For me, most of my deals are not hot when I invest. Hah. Often these companies go on to be hot later. But since I’m first check into companies when they basically have nothing, usually it’s just me and the founder’s mom who are investing. Writing the check is in itself the rapport-building activity.

2) You can assess founders better in person.

I also believe you can assess founders better when speaking with them in person. You can detect when there is co-founder tension / drama / something weird. You can detect when a founder is stretching the truth. All kinds of stuff.

I know this because I’m a super blunt / direct person. And, I’ve often called out things to founders directly. For example, there have been many teams over the years where I’ve noticed tension in a meeting between the co-founders. I’ve often pulled founders aside afterwards and mentioned my observations as such. e.g. “Hey, it seems like there’s some weird tension between you — are you having a lot of miscommunication?” And every single time, founders have broken down and admitted that they’ve been having some problems. You can definitely detect co-founder issues in an in-person meeting.

So given these huge benefits, why wouldn’t you meet a team in person? A bunch of reasons…

1) Unconscious biases.

It’s amazing how a team that is great at pitching can really “fool” you. There have been so many meetings I’ve taken over the years where you walk away from the meeting feeling really pumped and believing that the founders are amazing. And you think, “These are great founders!”

And then, I look back at my notes 24 hours later and re-read everything they’ve done or not done in the last few months, and you think, “Oh, this just sounds ok – they’ve only sorta achieved some things.”

Charismatic people can really fool you. Having charisma is a great trait, just in general. But, it can mask actual execution.

Moreover, charisma is cultural. What we find inspiring in a leader in the US is very different from what other people in other places of the world find inspiring. So, we have unconscious biases around what makes a charismatic leader. Extroverts, for example, in the US have a huge advantage. We generally think of extroverts as highly charismatic people. But extroverts are not actually any better leaders than introverts. There are plenty of examples of successful introverts who manage to inspired large groups of people towards a common goal. So we let our unconscious biases get in the way in assessing things like leadership because of the way our culture is set up.

One of my learnings over the years in venture is that it’s really important – as much as possible – to be objective. I try to assess what a team has actually achieved. Or what they are actually doing. But very often, meeting people in person detracts from assessing this, because some founders are much better at selling the dream and others are much worse.

There’s a well known top female VC who works at a very well known VC fund, and she was telling me a few years ago that one day her partnership heard 2 pitches. One of the pitches was by a woman who matter-of-factly just talked about numbers and growth and how she could build a big company. Another pitch was by a man who sold the dream and hadn’t done much of anything. After both meetings, the rest of her partnership talked about how they could really relate and build rapport with the male founder who was quite the visionary. This top female VC, however, realized that, although she was more excited about the male founder’s pitch, when she objectively thought about what he had accomplished, she realized it wasn’t much. And that the female founder had knocked it out of the park although her storytelling wasn’t as amazing. This story is a true story and this happens all the time in venture.

In the venture community today, we reward “visionaries” much more than executors. And a big reason for this is that we make investment decisions based on pitches rather than on execution (aka working) in our decision-making. This is a big problem and this is precisely what I want to change at Hustle Fund (though it takes baby steps).

The last piece about unconscious biases is that sometimes what we see in-person scares away traditional VCs. Such as pregnant women. Being a pregnant woman and pitching investors is NOT a recipe for success to raise money. Although there are plenty of successful female CEOs who have children while running their respective startups, it’s still not a positive sign to most VCs. This is a shame and something that is only noticeable / an issue when pitching in person.

2) Meeting teams in person limits your deal flow.

At the earliest stages, it’s important to see a lot of dealflow. If you are only doing meetings in person, it means that:

Companies can only be located in your geography

You need to spend a lot of money and time to fly to other places to see companies

You need to spend a lot of money to fly companies to see you.

If you’re a series B firm, all 3 of these can be fine limitations. You presumably have enough management fees to spend money on travel, and presumably, you don’t need to be seeing tons of companies in order to do great deals. But if you are at the earliest stages — such as a pre-seed fund like ours — you need to be seeing lots of deals and generally don’t have the budget to either do a lot of traveling or to fly companies to you.

And at the pre-seed level seeing lots of top-of-funnel deals is critical!

So, meeting teams in person is a tough strategy for small firms like ours — for both time / money reasons.

3) Technology is good-enough for remote meetings these days.

Technology is actually quite good these days. I think 10 years ago, vetting people through video conference might have been rough. But, today, Zoom.us, for example, is an amazing product for doing video interviews. You can see a lot with strong connectivity — including founder tension — and you can really feel like you’re in the room with the founder.

4) Meeting people in person is inefficient.

I don’t want to waste founders’ time and my time. The priority activity for them is in running their business. So for the most part, driving all around the Bay Area (in traffic!) is not a value-add activity for anyone. If we happen to be in the same place at the same time, that’s great — such as a conference / event / co-working space, but for the most part, commutes are a bear that I don’t think anyone should have to put up with if given the choice.

5) Lastly and most importantly, if you construct your portfolio in a certain way, it’s actually ok to miss things in a virtual interview.

After investing in hundreds of startups, I genuinely believe that it is much better to invest based on execution rather than to try to assess accurately based on talking. But, the entire industry is largely based on making investment decisions based on talking. This is a grave mistake, in my opinion.

Here’s an analogy in the job market — in the old days, you would interview a bunch of candidates. And then you would pick someone to hire largely based on talking. But as it would turn out — people who are great at selling themselves in the interview process are not necessarily the best performing hires! Business people have figured this out, and so these days, at so many companies, you no longer just talk in a job interview. Hiring teams now try to assess in other ways — through projects / short term contracts / tests / etc. In other words, execution-based tests are now used much more commonly to better assess hires.

In VC, the right analogy would be — why don’t we make a small bet for seemingly promising companies? And then try to assess based on execution whether or not to write a much larger check. (On the flip side, startups can assess us/me, to see if I’m living up to standards as an investor.) And as performers perform, let’s continue to do this. This seems like the much better way to assess performance — by actually assessing performance itself rather than talking.

For this reason, this is why I think it’s actually ok to miss some things in interviewing founders for a potential investment — because I care much more about how a team performs than how they talk & look.

Obviously both are important for a successful marketplace! But, if you want to build a really BIG marketplace, here are some observations from over the years.

1) Unlocking large amounts of supply matters A LOT!

This is a bit unintuitive. Most people who set out to build a marketplace think that if you can get people to pay for something (the demand side), then you’re all set. I’ll argue that it’s certainly important to test the demand side but it’s almost more important to test how hard it is to get supply.

From my experience in growing an ad network, it is possible to have lots of demand but not enough supply! This is actually a very common phenomenon. Case in point, most email newsletter companies have an easy time selling out their ad slots, but it’s incredibly hard to continue growing an email newsletter at a fast clip. The way that a lot of email newsletter companies solve for this problem is by introducing new lists with the same audience. E.g. you can receive the daily news digest and also the daily jobs email. This gives them twice as much supply with the same audience.

2) If you are aggregating supply, the key is to unlock new supply

One of the big areas where I see marketplaces fail is by going after an existing market and trying to amass the same supply that already exists. So for example, a marketplace for salons or a marketplace for wedding venues or a marketplace for co-working spaces. These marketplaces are all amassing existing salons or existing wedding venues or existing co-working spaces. These are existing places that consumers could ordinarily find themselves and pay for directly. You are literally just moving supply around and not growing it. The issue with doing this is that this existing supply already has certain expectations for payment, because they are already making money for this service or asset that they provide. This then makes it hard to be a middle(wo)man and take a cut in between. You are competing with a strong alternative — to be found directly.

The better way to aggregate supply is unlock new unique supply. Airbnb is a great example of this. People were not already using their extra bedroom as a hotel room or their couch as a bed. They don’t have the same expectations around making a ton of money unlike the Holiday Inn. Airbnb has effectively brought a ton of new “hotel room supply” to the market that didn’t exist before. They were not try to resell existing rooms in existing hotels. Uber and Lyft are equally good examples of doing this in the taxi market. They brought into the taxi market new “cab supply” that didn’t exist before, and these drivers don’t have the same expectations for monetization as existing taxi drivers.

Ultimately, unlocking new supply drives demand. If I can stay on someone’s couch next to the Moscone to attend a conference for 50% of what I’d pay for a room at the Holiday Inn, I’d do it. You are reducing prices for the end user by unlocking new supply, and this drives demand.

So going back to the original examples of marketplaces for salons or wedding venues, etc, can you get clever / creative in creating new supply? Can you turn new people who are not in the salon business into a salon owner? In many cases, doing this might just be too high of a cost and not possible, but in some cases, this approach may be a good strategy. A good example of this is Wonderschool. Wonderschool is turning people into new daycare owners — they are not amassing a network of existing daycares but rather unlocking and creating new ones to add to their network. So think about unlocking new supply rather than moving existing supply around.

3) The unit economics need to work in the long run at scale

Once you initially test both supply and demand, there’s going to be a constant tension between both sides. Sometimes you’ll be supply constrained. Sometimes demand constrained. Often, it may not be clear if the unit economics will work out while you’re building this up.

In fact, ridesharing companies often get a lot of flack from the public, because they are not profitable yet. But, the holy grail for them is autonomous cars. Once these become mainstream, they will have access to infinite supply at a low cost. So while the short-term numbers may be questionable, the long-term future of these companies seems very promising.

Similarly, you’ll need to think about what your long term control over supply will be. Most marketplaces that are successful have a stronghold on at least a good portion of their supply to help with pricing pressures. Successful ad networks are a great example of this — Google may run a large ad network across many properties they don’t own, but they also own a lot of their own properties including Google search and YouTube. Likewise, although Airbnb doesn’t own properties today, it’s rumored they are going into real estate. So once you get some footing on your marketplace, the next question is how can you think about controlling your future by having access to or creating at least a good portion of your supply?

4) What should I look for in amassing unique supply?

If I were to build a large marketplace today by amassing supply, I would start by looking around at what is currently wasted (space / time / assets). Then, I’d think about how this wasted stuff might be cleverly transformed into something else that consumers and businesses currently spend a lot of money for.

Summarizing all of this, to make a marketplace fly, you need to cleverly come up with a LOT of unique supply (obv there has to be demand). 1) Turn something else into supply where people don’t have high monetization expectations (Airbnb, Uber, Lyft). And/or 2) eventually you own it or part of it (e.g. scooters / Google search).

At Hustle Fund, we talk a lot about speed of execution. Part of this is grit and founder hustle. But what most people don’t realize is that speed is also baked into the business model itself.

For example, one of the things that people don’t realize is how much sales cycles and payback periods matter. As a concrete example, fast growth direct-to-consumer companies are now able to go from $0 to $1m revenue within a month or two with just < $25k in ad spend. This is incredibly fast — unprecedented and very low cost.

How is this possible? All because of fast sales cycles. Let’s dive in:

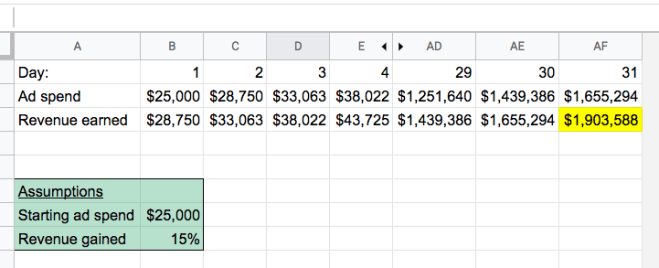

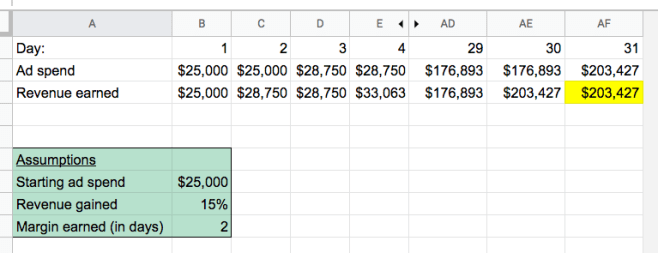

Let’s start with a simple example. Suppose the following:

We start with $25k in ad spend on day 1

As soon as people click on our ad, they buy immediately and we get that revenue immediately

For every $1 we spend on our ads, we make an average $1.15 in revenue

We pour everything back into ads the next day

You can see that within a month, we are at an almost $2m revenue generated with just initial ad spend of $25k! This is crazy. You can raise a small pre-seed tranche and get to Series B benchmarks within a month.

Now, in practice, the scenario I’ve outlined is near impossible. Namely, most of the time, your ad spend is not this effective on day 1 and often requires iterations and testing. Moreover, it often takes some time to clear with your payments provider even if you generate revenue right after someone clicks your ad.

But this scenario is actually not that far off from what many of the direct-to-consumer incubators are achieving.

Ok, let’s add some delay to make this a bit more realistic. Let’s suppose:

We start with $25k in ad spend on day 1

As soon as people click on our ad, we do get our initial ad spend back immediately but we don’t make any profit until the even numbered days

For every $1 we spend on our ads, we average $1.15 in revenue (on the even days)

We pour everything back into ads each day

This is a contrived example (profit only on even numbered days?? weird.), but you can see in this example, we went from a near $2m revenue generated at the end of the month to just a $200k revenue generated, even though the delay in our profit is not that long. Not only that, we are making about half the profit as before, but our revenue generated has now dropped by nearly 10x. Why? Because time is a compounding factor.

So when investors are concerned about sales cycles and payback times, this is what they mean. Regardless of whether you are using ads to get customers, if you calculate this out, you can see how just small affects in sales cycles / payback periods hurt you big time. The other thing is that as an entrepreneur, you’re working just as hard in the first scenario as in this one, but your sales are affected 10x.

Both of these examples are still a bit contrived, because as I mentioned above, you usually don’t know if your ads — or any of your customer acquisition channels – are working (they probably aren’t) on day 1.

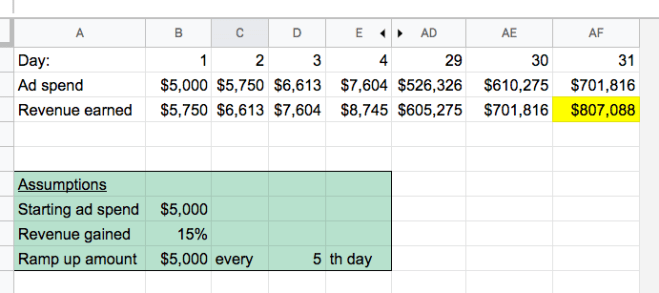

So now let’s assume that you don’t start with $25k in ad spend. Let’s start with $5k. Suppose the following:

We start with $5k in ad spend

As soon as people click on our ad, they buy immediately and we get that revenue immediately

For every $1 we spend on our ads, we make $1.15 in revenue

We pour everything back into ads the next day

We add an additional $5k in ad spend every 5th day

You can see that with this example, we can get to near $1m revenue generated by the end of the month ($800k+). In this case, we end up spending a bit more on ads, but this is a more gradual (and realistic) approach to ramping up ad spend. Again, in this example, because we make the $1.15 for every $1 immediately, you can see that this helps us achieve greater revenue than in the prior example.

In your own business, how can you decrease your sales cycle + payback period by even just 10%? How can you increase your margins by even just 5%? These all add up significantly as you can see over short periods of time.

The tl;dr is never underestimate the value of time in making money.

I debated writing this. Partly because I didn’t want to jinx my portfolio. Partly because my gains are all on paper anyway. And partly because when I did my angel investing, it was at the beginning of my investing career when I really didn’t know what I was doing. Hah.

Nonetheless, I do think I’ve had some great learnings that are worth sharing with entrepreneurs and would be angel investors.

1) You don’t need to invest a lot of money to become an angel investor.

I think a lot of people think of angel investors as super rich, investing $25k-$100k at a time. This is what I thought too when I was an entrepreneur. I thought, “Someday, when I get to be super rich, I’ll start angel investing.”

Later I learned that actually a TON of entrepreneurs in Silicon Valley angel invest. And they are not even that rich. How is this possible? I would later meet a number of entrepreneurs who invest $1k-$5k checks into startups.

That was a mind blowing discovery. You don’t need to be filthy rich to angel invest. Just like how there are now microfunds. There are microangels.

2) Being an angel investor helps you network

The second learning was that entrepreneurs who are angel investors can mingle and network with fellow angel investors. This allows you to build friendships and rapport with other investors who have more money than you and guess what…they can invest in your company and introduce you to other investors!

This is a great strategy for raising money that I wish I had known when I was building my company.

3) Your small check size doesn’t matter if you are value-add.

You might wonder why any entrepreneur would even accept such a small check of $1k. If you can be value-add, then that really helps you win deals. Because more than money, people want help. Especially at the earliest stages. Think about it — money buys help, so if you can provide help for free, then that’s huge.

Do you know something about engineering? Marketing? Sales? Design? Do you have a good network? Can you provide good feedback on things like marketing materials / landing pages / pitch decks? These are all value-added activities at the earliest stages that help you win deals when you are writing small checks.

4) Your reputation matters most.

A lot of new investors inadvertently are a pain to work with. I hear stories of people who take 5 meetings for just a $25k investment. Or stories of investors who require tons of due diligence for a $10k check, including 5 year spreadsheet projections and extensive business plans.

If you’re new to the game, set expectations for what your process will be like. Be transparent. How many meetings do you typically need to make a decision? Do you want to mentor the company first before deciding? Whatever it is, be transparent with your process so that the founder can decide whether or not he/she wants to go through with your process.

Reputation matters and word gets around very quickly. This will set you up for future deals.

5) Work with founders lightly to learn

Like everything else, investing requires practice. And the only way to practice is if you have a feedback loop. You need to work with your founders after investing in order to better understand what type of company you picked and understand what’s going on in the business / with the founders.

Make sure you are not a nuisance. See above. You don’t need to work with the founder forever. It could be a few meetings to help them with their deck. Or it could be a few meetings to help them with their website. Or UX of their product. Or product testing. But you need to interact with the founder so that you can get better at picking companies.

An alternative to becoming an angel or microangel is to work at an accelerator or incubator. Or even mentor as a volunteer for an accelerator or incubator. You will learn a lot about teams and different kinds of businesses. Accelerator programs see a TON of deal flow and invest in a lot of founders, and you will learn a LOT about investing without risking your own money very quickly.

6) Build a large diverse portfolio

VCs often debate whether you should have a “spray-and-pray” portfolio vs a “concentrated portfolio”. Having built both kinds of portfolios before, I think building a “spray-and-pray” portfolio is the easier strategy to start with.

What do these terms mean?

“Concentrated portfolios” — these are portfolios that have a few number of companies — say 10-20 in total. So if you are allocating say $100k in total to angel investing, you might put $10k into 10 companies. Most Sandhill VC funds are in this camp.

“Spray-and-pray portfolios” — these are portfolios that have a lot of companies in them — certainly 20+ and some cases 100+ companies. So if you are allocating say a total of $100k to angel investing, using this strategy, you might put $1k into 100 companies. YCombinator and 500 Startups are examples of this approach.

A lot of investors have strong opinions about which is the better approach. Having looked at the data, you’ll see big winners and losers utilizing each strategy. So, like everything else, it’s really a matter of how good and lucky *you* are.

I think the spray-and-pray portfolio strategy is easier to start with, because there’s room for a lot of error. Your initial investments will likely be horrible, because you won’t know what you’re doing. This method gives you a lot of shots at trying to capture a super huge winner, much like how YC has Airbnb and Dropbox.

Statistically speaking, if your sample size of deal flow is “generally good” and you are an “ok picker”, you can at least get to at least breakeven with the spray-and-pray strategy. A former colleague of mine Matt Lerner, simulates this nicely in a post on the spray-and-pray strategy.

The tl;dr is that in essence, if you have a portfolio of roughly 100 companies, you should be able to pick at least one company that is 100x+ return or higher to get your portfolio to breakeven. For each additional startup that is 100x+ return, your overall portfolio will yield an additional multiple. E.g. if you have 3 100x+ returning companies, you’ll have roughly a 3x portfolio multiple.

The question about this strategy that I often hear is whether it is possible to generate say a 50x returning spray-and-pray portfolio? And the answer is yes – YC is a good example of that. To achieve this, you must have at least one deca-unicorn (like Airbnb or Dropbox) in your portfolio.

So if you go with the spray-and-pray strategy, you can start to build this over a few years — invest in say 5-10 companies per year to end up with 50-100 companies in your portfolio. Each year, as you get learnings, hopefully your dealflow and picking gets better.

7) Be patient and don’t freak out.

You will want to freak out in the beginning, because you will see a lot of seemingly losses. This makes sense because the companies that can’t make it will die earlier than later, and the big winners that will return your portfolio won’t get to maturation until years later. So you need to have some faith and a strong stomach. You won’t see your portfolio start to inflect for years!

I was a microangel from 2014-2017 (I no longer angel invest because I now run Hustle Fund). I invested in 7 companies over those 3 years with $5k checks in 5 of them and $10k checks in 2 of them. 3 of these companies shut down more or less before I had paper gains on the others. So it was incredibly nerve wracking, because I felt like I was losing all my money!

8) Be prepared to lose all your money!

All of this said, you can always lose all your money. So, be prepared to do so. Angel investing is risky, and most angel investors (and VCs!) do not see positive returns. Don’t part with more than you can handle.

And this brings me to my next point.

9) Investing is all about power law — don’t worry about your losses.

In talking with a number of fund managers and seeing data from my own experience, you can basically think about your portfolio companies in 4 buckets.

Most of your companies will fall into category #1. And that seems scary. But, as you can see from my portfolio, your losses don’t really matter. In fact, if you copy this sheet and play with the numbers, you’ll see that your low returners don’t matter either! Everything is really riding on your excellent returners, which you won’t have many of.

A few takeaways from this spreadsheet of my angel investments (and please do copy this and play with the numbers):

A) You need at least one excellent returner. I often hear angels talking about looking for 10x returns or 2x returns from their companies. As you can see, you need to be shooting for much much higher in your ultimate winners.

B) Your good returners don’t have as much impact as one might think unless you have a whole handful of them.

C) New angel investors worry about the losses and sometimes get nasty with founders who lose their money. But in practice, those losses don’t matter either. If you get nothing back vs $0.20 on the dollar, it’s a wash — it’s literally all the same.

Of course, it’s always nice to receive money back from a company that is winding down. I see that as a good signal about the founder — that he/she is looking out for your interests and wants to do right by you. But as you can see, from an ROI perspective, that dollar amount itself in that category really doesn’t matter.

In contrast, seasoned investors don’t care about the losses and concentrate on the potential winners. You need to try to find as many of those 100x+ returning companies as you can — that is what the game is about. This is something to keep in mind as an entrepreneur — how can you convince someone that you are a 100x+ winner?

D) You won’t know who in your portfolio is the excellent returner(s) when you start investing. And you won’t know for years.

My portfolio is 3-5 years into angel investing, and all of this is paper gains. So all fake gains right now. Any one of these companies could go belly up at any time. The hope is that one of these companies can inch up to 100x real gains. But we’ll see.

10) Start by co-investing with people who have good deal flow

In the beginning, you won’t have a brand or deal flow. The easiest way to jumpstart your angel investing is to find people who do. Find friends who already have been investing for years and have been doing well. You can also invest in funds, who may share their deal flow and pro-rata rights. Or you can mentor at accelerators or co-working spaces.

Once you start generating deal flow, by continuing to invest, you build up a brand over time.

You will want to see a lot of deals in order to start to compare companies to each other. Seeing a company in isolation won’t help you understand if it’s a “good company”.

You need to understand whether the team is in a competitive market — e.g. are you seeing 10 companies chasing the same thing? Do you place a bet after seeing a lot of companies or do you shy away from the space altogether?

You won’t know if a company’s revenue growth is good or not until you see other companies and their growth. The other benefit to being an angel-entrepreneur is that you get to see what is “market” as far as competitive spaces go and growth rates go. You don’t normally get to see that as an entrepreneur. That helps you understand how your startup stack ranks.

11) Entry and exit points matter

One of my most surprising learnings from investing the last few years is how much entry and exit points matter. I learned that there are a lot of investors that brag about investing in marquee companies that have done phenomenally well and yet have made little to no money because they got into a deal at too high of a valuation and got out at a valuation that isn’t high enough to cover their other portfolio loses and make money.

Unfortunately, as an angel, you have no control over the exit point. You are just along for the startup ride. So you can only control the entry point.

So for example, if you are shooting for 100x+ multiples in your winner(s), then if you are investing at $3m cap on a SAFE, then roughly speaking, you are trying to exit around the $300m valuation mark (or higher!). If you are investing in another company at $6m cap on a SAFE, you need that company to deliver 2x the exit of the first company, which is incredibly hard. Note: historically, the number of new companies that get to the $1B valuation mark each year was less than two handfuls WORLDWIDE, though in the last couple of years, hundreds have been promoted to unicorn status in the startup bubble.

So maybe your strategy is to invest at a low valuation. Maybe it’s to invest in high valuation companies run by high profile founders. But whatever your strategy, entry and exit points matter.

12) It’s all luck. No one can spot a winner at the earliest stages.

One final thought — angel investing at the earliest stages is pretty much luck. Anyone who tells you it’s skill is sh*tting you. You can have amazing founders do amazing things and then get run over by a bus or have some regulation come in and break up the party. And if you’re riding on just your one winner covering your loses and delivering big gains for your whole portfolio, that’s a lot riding on one company. Maybe you have a couple or a few of these winners, but if one falters, then that reduces your multiple by a point or so on a portfolio of 100 companies.

So your best investment is probably to buy a magic 8 ball.

To recap:

-Risk capital you can afford to lose

-Learn from your investing and improve your thought process and strategy

-Microangels are en vogue and being one helps you access other angels

-Structure your portfolio to diversify enough to increase your odds of capturing at least one big winner (at least 50 companies if not more to get a winner of 100x)

-Keep entry and exit points in mind

Here are some things that I think will be big in 2019:

1) Furthering vocational education

I think traditionally, a lot of investors have been shy to invest in education. In US, let’s be honest — we don’t really care about education! Here’s a good post that my friend Avichal Garg wrote on the education landscape several years ago which I think still applies today in the US.

But the tide is changing a bit. Specifically, what we’re seeing in the US is massive student debt. And new college graduates are not able to get a job or a high paying job. For so many people in the US, if you are not majoring in a STEM subject, it probably does not make sense anymore to go to college. Period. The economics of college are just terrible.

So while we don’t care about education in the US, we do care about business and return on investment! And it does make sense now to provide education of “useful” topics for the workplace — for a job, for livelihood. This is why we see the rise of Lambda School which ties your livelihood outcomes to your cost of education. And there are many other schools that are cropping up such as Make School and Kenzie Academy (we are investors at Hustle Fund) that are trying to teach useful topics that you can actually use and are willing to pay for, because you can use those skills to make money.

I think we will see a lot of new businesses stemming off of this trend.

We’ll certainly see more schools — both in-person and online covering more topics. Everything from coding to digital marketing to sales to even entrepreneurship. But also vocational categories as well. Can you teach medical skills or plumbing skills using VR headsets remotely?

Additionally, I think there will be businesses stemming off of these. Lots of new ways to loan money to students. New ways to provide socialization and networking for remote students. New real estate opportunities for these students.

2) Improving commutes

Commutes are terrible! (and a big waste of time). This year, we will see a lot of businesses built around making your commute better. Commutes can get better in two ways: A) By actually reducing your door-to-door time and B) by making the experience while commuting better. We’ll see opportunities in both.

A) There will be new ways of commuting in less time.

This is really what the rise of Bird and Lime is all about. When it’s faster and cheaper to go from say SOMA to the Financial District of San Francisco by scooter vs car AND is accessible to everyone, people will do it. In contrast, not everyone can ride a bicycle or a skateboard (e.g. more expensive, need balance or skills – not accessible to all)

But scooters really only work in warm-ish places where there are bike lanes / wide enough roads. E.g. places where it snows / places that don’t have bike lanes won’t be great markets in the long run. So there’s an opportunity to come up with a mode of transportation and model that can withstand weather / lack of bike lanes. My guess is that we will just see further advancement of ridesharing combined with autonomous vehicles. An early version of this might be effectively new autonomous bus lines that just go up and down streets continuously. This is already starting to happen in some cities.

B) As people drive less, they will have more time during their commute

This is a big opportunity for people to do more work, shop, and play more too. For example, we’ll likely continue to see growth in podcasts and tools for podcasts this year. Spotify made clear that they believe in this opportunity by announcing two acquisitions in podcasting this week.