For many years now, VCs have absolutely “hated” investing in media companies. If you were starting a blog or a newsletter, it would be very challenging to raise money from traditional VCs unless you had proven out a ton of traction (with a fast growth trajectory).

But I think it’s important to understand why, because we’re starting to see an inflection point that will shift the entire industry.

Side note: my view on this topic is fairly strong and comes from working with a lot of newsletter companies over the years in running my startup, which was an email ad network.

What’s wrong with media companies?

VCs typically have not liked these criteria about media companies:

Low exit multiples on ad revenue (often 1-2x on annual revenue) Hard to acquire users quickly & scalably (CAC is too high at scale) In a recession, companies reduce ad spend – especially brand advertising

All of these things have been traditionally true — especially if you’re looking to sell your business in 5 years.

But what if you thought more long-term? Not a 5 year horizon but 10-20 years or even 20-30 years out? How would you think about your business differently? What would your strategy be?

Regardless of your business, you might do something like:

Gather an audience – maybe start a newsletter to get loyal fans Launch a product to that audience Launch many products to that audience to upsell them etc..

And maybe you sell ads or event tickets in the beginning to provide cash flow and keep your company afloat, but eventually you start selling other products and services to a loyal group of people… Maybe you even start a fund that gets layered on top of that.

Oddly enough, that playbook looks like starting a media company!! This is what is happening now — you see creators and influencers starting media companies with long-term goals in mind.

People like Mario Gabriele with The Generalist and Packy Mccormick with Not Boring (full disclosure: am a small investor in his fund) are layering on lots of programs and monetization mechanisms that all work in tandem. E.g. content about companies can also be investments and vice versa. When you align community engagement with monetization, this allows for incredible scale. I would bet that Alexis Grant’s new company They Got Acquired could very easily follow the same playbook with a similar audience.

Why now?

Now you may be saying, “Well media companies have always tried to mesh together different monetization methods to try to increase value. Why is now any different?” For example, Thrillist acquired e-commerce company JackThreads to try to increase monetization.

I think now there is just so much more infrastructure available to media companies to enable them to quickly plug into new monetization methods and tools. For example, Angellist’s rolling fund allows creators such as Packy to quickly spin up a fund without doing the time-consuming backops work and fundraising required for a traditional fund. This didn’t exist even 2 years ago.

Or other wildcards — like crypto. Mario created NFTs — without third party tools to do that quickly and without hassle would make this near-impossible for a media company with limited resources to do at scale. You can envision community tokens coming in a big way to incentivize audience members to get more engaged and contribute.

In other words, there are now many ways to monetize quickly that have much lower COGs than creating new physical products to sell.

I think there has never been a better time to start building a media company and we will see many billion dollar media companies coming out of this era — perhaps even run by just a handful of people. Long gone are the days of just ads and events — the bigger monetization mechanisms are just getting started.

I think we’re seeing a very big shift right now in how startups are created and operate. But before we dig into that, I want to spend some time talking about work.

For centuries, work has been incredibly inefficient. In the “barter era”, one person would do work in exchange for someone else’s work. E.g. I’ll make you a silver fork in exchange for salt and spices. There were many things challenging about this type of economy. 1) There was no common currency to transact and understand value, and 2) on a macro level, it was hard to know whether your good or service was really needed and whether it was going up or down in value. E.g. Is there a surplus of spices? Should I be spending time in spices or something else this year?

Money came along and solved the first part of that problem. Tribes and groups of people adopted currencies that are the predecessors to modern day money. You could carry around some form of fiat and use it to buy things. You could sell your goods and services for fiat. This helped standardize commerce.

Eventually, the Medici family in Europe established ledger-based banking so that you could take your goods and services to one location in Europe and it would be good for a credit that could be used at another Medici bank. Coincidentally, around the same era, the Yap money system in Polynesia had similarities where money was actually represented by large stones, and there was a record of who paid with which stones. The large stones were too heavy to be moved, so the pointers of who owned those stones did were written down on a similar ledger-based system.

Money solved fungibility issues. But it never really solved the latter problem of understanding where your good or service fit into the broader landscape of what is actually needed in society and how it was valued.

And for centuries after establishing complex monetary and lending systems, this problem still came to a head often. In 2000, during the dot com bust, it became clear that tons of people built out companies and products that no one wanted. Overnight, many of these companies went to zero and many people in the internet industry were laid off. Time and again, we’ve seen companies hire up the wazoo only to do massive layoffs of employees who gave their whole lives to a given company.

In fact, as an individual worker, you often don’t know if a layoff is coming. You often don’t know if things are going well / not going well within your own company. Management typically doesn’t tell you. As an individual, you also don’t know if you should be taking this job or this other job, because beyond the salary, you don’t really know what it’s like to work at a given company until you start working there. And traditionally, you’ve only really been able to work at one company at a given time.

This brings us to today. As of writing this in 2021, mobilizing money isn’t the number 1 issue for companies. It’s attracting and retaining talent. Now you may be thinking, “Well that’s nice and all but I’m still having trouble raising money for my startup.” I have 300+ portfolio companies at Hustle Fund – all with varying degrees of fundraising troubles. But all of them — even once they have the money — are in a war for talent. Even the most well-funded companies who are no longer startups are having trouble finding and retaining talent.

Folks, the current way that startups are being created is starting to break. Under the current way of building startups, you have to figure out what potential users want and will pay for by doing customer development, pitch investors who are not your customers / don’t get it / are traditionally slow, fight in this war for talent against Google, and lastly, as a founder, get burnt out and combat personal mental health issues in the process. Does that sound like the best way to deploy resources for our society?

But what if we flipped startup-creation on its head? What if you start with a mission and values — not founders? For example, at my company Hustle Fund, our mission is to democratize wealth through startups. And to that end, we are furthering capital, networks, and knowledge in startup ecosystems. Even though I’m a founder of the company, it doesn’t matter if I personally work at Hustle Fund or not. It’s the mission that’s important and the people who want to work on that mission. And if no one cares about the mission, then the organization shouldn’t exist regardless of what I, as a founder, think about it.

And if you start companies with missions instead of with founders, then you start to attract people who have lived and breathed that mission before. Those people really get it. And those people are also would-be customers or users. And maybe these same people are not only working on this problem together in a cooperative way but are also investors in the problem — both through work and capital.

When you start with organizations that are centered on missions, then you start to chip away at existing startup problems. Such as understanding whether you’re building something people want – your colleagues are also your customers. They are also your investors and are more value-add through their feedback and network. You also solve for mental health issues. Founders often feel like they *have* to stay at their own company because there is often no one else to lead in the early days.

For all of these reasons, this is why I think we’ll see the rise in the decentralized startup. In fact, we already see many Decentralized Autonomous Organizations (DAOs) in play — this is not a new concept and DAOs are precisely what I described above.

Magdalena Kala tweeted a few articles on DAOs that I think are really good and are all worth reading if you’re not that familiar with DAOs:

DAOs, of course, are not immune to the fight-for-talent problem. But, unlike at a traditional company, often you’ll see various people working on goals or milestones for DAOs in a part-time way. Traditional companies often require their workers to sell their soul to their organizations. But, DAOs mostly just care about getting stuff done. And the transparency around what is happening in the organization gives everyone a clear picture of where a project stands, what is happening, and who is doing what (and getting paid what). In a traditional company, most of this is opaque. You can see if a DAO is going well, but in contrast, you really don’t have a clue with a traditional company.

A DAO that I think is really interesting is the Friends with Benefits DAO (h/t to my business partner Shiyan Koh for showing me this). It’s basically a membership club of inclusive thinkers and creators. They list their values upfront, and people who resonate with the mission can pay (invest) to join the group. This in turn becomes a community that funds the mission, and over time, as they build and monetize, the community who is also their customer base, will benefit. This is the ultimate — having your investors and customers wrapped up as one.

I think we will see many more DAOs formed in the coming years, and reiterating what I mentioned in 2018, I do think that some form of crypto will disrupt traditional VCs over time. But I also think decentralized startups will start to appear even without “typical crypto components”. There will be startups formed around missions that don’t start with founders nor involve crypto but have radical transparency. There may also be decentralized startups formed without Discord channels (personally, I’m unclear how anyone, myself included, can do deep work anymore with so many Discord channels) and just rely on wikis / Notion pages / Mirror / etc to document what work is being done without minute-by-minute chatter. I think we will see startups formed with people who work at multiple places simultaneously or are all contractors – such as how Gumroad is set up. And in that scenario, the need to raise so much money for the company actually becomes *less important*, because you don’t always need funds to cover someone full time and compete with much crazier full-time offers from FAANG companies. This mitigates the fight for talent issue.

At my own company Hustle Fund, some of these concepts are things we’ve thought about and have experimented with a bit. We’re not quite a DAO, but we are a bit DAO-like. We have a number of talented people who are part-time because they believe in our mission, and we are excited to be able to work with them in any capacity. Our GMs also have a ton of autonomy with their business lines that align with our mission — I often don’t have the foggiest clue what is happening with the day-to-day on their businesses, and that’s ok. In fact, that’s great. So at Hustle Fund, which is completely distributed, we have leaders of different facets of our mission who reap strong upside when their particular projects go well. In many ways, a structure like this requires working solely with entrepreneurial people – people who enjoy running with things without centralized instruction or authority.

Ultimately, the most ideal working environment for an individual is to be able to work on a mission (or many missions) you love with people you enjoy. You’re happy with your compensation and feel like you have strong autonomy to be able to have an impact. You get crystal clear transparency get be able to make good decisions for both the organization you work for as well as for yourself personally. This is what I think most people want for themselves and their families, and why I think we’ll see the rise in decentralized startups in the years to come.

It’s hard to believe that we’ve been in the pandemic for almost 1.5 years now! But the silver lining of a pandemic is it really forces you to question what is important. One of the thoughts I keep coming back to is around mission and purpose, which I wrote about last year at the start of the pandemic. AKA, what are you doing with your life and why?

When we started Hustle Fund a few years ago, setting out to make a boatload of money was not the (sole) purpose of the organization. Prior to Hustle Fund, I could have worked at a number of top VC funds that could have set me on a clear lucrative path. But I wanted to do something bigger and more impactful — something that would also help a lot of entrepreneurs. In mapping out Hustle Fund almost four years ago, we decided that core tenets to our mission at Hustle Fund was to further capital, knowledge, and networks in startup ecosystems.

Recently, we had a chance to reflect on how we’re doing against these tenets at our Hustle Fund team offsite.

Mapping out the future of Hustle Fund

At Hustle Fund, we believe that great founders look like anyone and come from anywhere. In the last four years of Hustle Fund, we’ve built scalable processes to fund nearly 300 pre-seed companies globally! Even pre-pandemic, we made almost all of our funding decisions online through video conference calls. We’ve invested in approximately 50 companies off of cold-application forms.

We’ve also spun up Angel Squad led by Brian Nichols, which in its first year alone has deployed ~$10m into startups of all sizes! Both our pre-seed VC fund and Angel Squad are on their respective ways and continue to build momentum everyday.

And beyond Hustle Fund, a lot of our peer VC funds now do the same. While it’s never easy to raise money, entrepreneurs who are not well-connected can now raise at least some capital remotely from connections built entirely online. And it doesn’t have to be from VCs. In the last few years, we’ve seen the rise of crowdfunding, roll-up vehicles, angel-operator syndicates, debt and revenue-based financing options. Startup capital is what made Silicon Valley special for so many decades, but these days, the capital markets for startups has largely opened up and continues to move towards a free-market dynamic — which makes capital more accessible.

But, Silicon Valley is still a special place for knowledge and networks. Successful entrepreneurs here have long shared advice to the next generation of new entrepreneurs behind closed doors. Tactical advice on things like customer acquisition, hiring, fundraising, testing quickly, building teams and keeping morale up have been passed on from one founder to the next.

At our offsite, we realized there’s a lot of work to be done in opening up knowledge and networks. In this next chapter of Hustle Fund, just as we’ve pushed hard (in a small way) to open startup capital markets, we are going to start pushing to make startup knowledge and networks accessible globally. Unlocking the secrets of startup tactics and inspiring stories is the beginning of what you’ll see from us.

To kick this off and give you a taste, my business partner Eric Bahn will be doing a fireside chat with Vlad Magdalin, CEO/founder of Webflow. In this fireside chat, the two will share stories of what happened in the very beginning, before Webflow became a unicorn.

This will be an amazing event – *open to ALL*! @callmevlad is a wonderful person! He also was a refugee & grew up cleaning offices at night. He will talk about building @webflow from 0 to unicorn, & @ericbahn will try to laugh at (or augment) his bad dad jokes. https://t.co/l35rsaHHdO

If you read the funding stories of Webflow, on the surface, it looks like it was a walk in the park. But the Webflow story could not have been further from that.

Vlad exemplifies what the American Dream looks like at its best. As a refugee to the United States from the USSR, he cleaned offices at night with his family to make ends meet while growing up. He also started Webflow in 2005 but had to stop many times along the way to take jobs to earn a living. Eric and Vlad will talk about those tough early days of the company in a way that most startup stories are not portrayed.

This event is free to all and will be next Tuesday evening PT – I highly encourage you to attend and stay tuned for much more!

The tl;dr for my last post is that these days geography is rather confusing. It’s quite common for a San Francisco Bay Area company to start hiring from day one an engineering team that is elsewhere and building up a real hub elsewhere even though everyone sees them as a San Francisco company. Or for a startup located outside of the US to sell to US companies. The world is a lot smaller than it used to be.

And so for these reasons, I believe that to start a company, you can start building a startup these days from pretty much anywhere. The most important thing in the earliest stages is to try to get to product Market fit quickly.

Knowledge has become commoditized at the earliest stages – you can pretty much read about Lean Startup anywhere on the internet. But what about scaling a business?

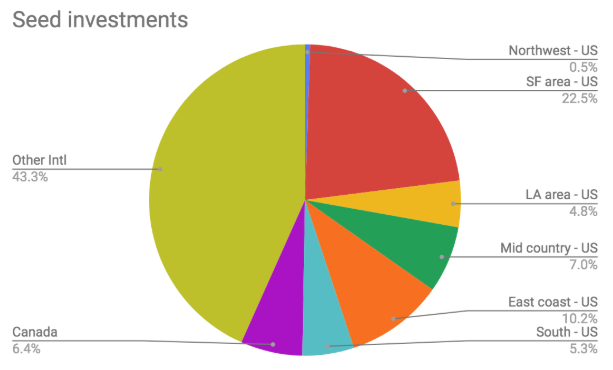

The numbers are actually pretty sobering. I went ahead and graphed some interesting fundraising data from past portfolio companies that I’ve invested in either as an angel or as part of a team where I was a/the decision maker.

I took my whole portfolio of all companies that I had invested in between 2014-2016 and created pie charts based on geography. N = over 250 companies in this dataset.

You can see the vast plurality of companies that I invested in during this time were largely international companies Note: for the purpose of this exercise, I separated out my Canadian startups from the rest of the world. (Canadian startups are so similar to US startups that I thought they deserved a category of their own.)

I did the best job that I could in labeling just one geography for each startup, but this exercise was a bit tricky. For example, a company that I had invested in is categorized as a San Francisco-based company even though the vast majority of their employees are now based in Dallas. The reason for this is that when I invested in them, the founders were and still are based in San Francisco, and the bulk of their decision-making and operations were happening here at the time. On the flip side, I classified a number of companies whose founders had recently moved to the US from another country and were doing significant operations in that other country as “other int’l”, even if they were US Delaware C corps. As you can see per my last blog post, it gets a little bit complicated.

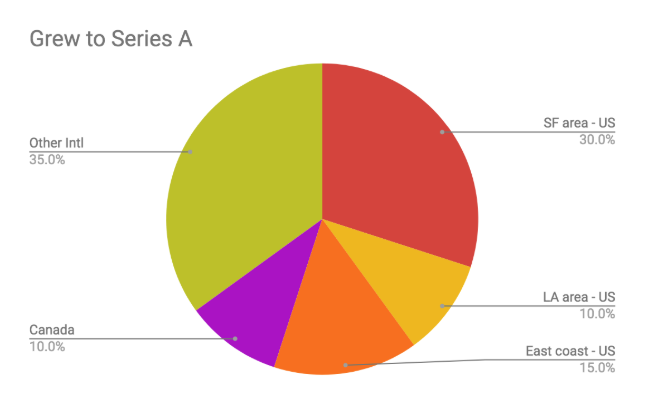

I then went ahead and grabbed the companies that made it to the Series A level and graphed what the breakdown of those startups look like by geography. The reason I say Series A level is that I have a number of portfolio companies who have done well in revenue and have not had to raise larger rounds. So if a company had raised a series A, I labeled the company as a Series A company regardless of where the raise happened. Now, I understand that there are some issues with the nomenclature because a Series A in the Bay Area is so much later than a Series A in say Australia, but, this was the best I could do. In addition, if a company had not raised a Series A but had hit US Series A milestones – namely $2m+ “net revenue run rate”, then I counted the company as a Series A company.

What is interesting about this graph is just how much the percentages have changed. Let’s come back to the analysis in a second.

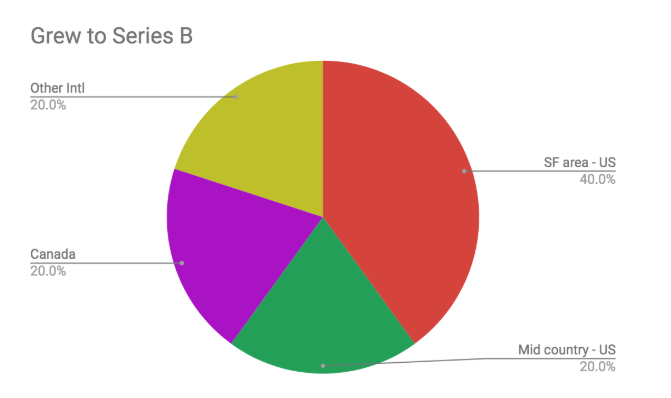

I went ahead and did the same exercise with Series B companies. I graphed my portfolio that had graduated to the Series B level. And again, for companies who raised a Series B – whether here in the US or abroad — were labeled a series B company. For companies who had hit US Series B traction milestones – namely 10m+ annual net revenue runrate – I also added those companies to this category as well.

You can see that this graph has changed even more.

Here are my takeaways:

1) The San Francisco Bay Area punches above its weight. (not surprising)

One could try to argue that perhaps my San Francisco Bay Area founders are stronger. While I couldn’t tell you whether that’s true or not, intuitively, my gut feeling is that that is not the case.

What I do think is happening here is that the San Francisco Bay Area has a lot more capital, and so there are more startups that get more funding than in other parts of the world. And by proximity of being here, it is easier to access the capital (even though there is also more competition).

But the other thing that I think is happening is access to talent and knowledge, especially as companies scale. I tend to invest in businesses that require less capital. This tends to skew towards B2B companies or other businesses where the margins are nice. I tend to prefer investing in companies where if they could never raise a dime of VC funding again, they would still be able to survive and thrive.

And I’ve applied this lens across all geographies. So as a result, I would not expect such wild differences in ability to get to the Series A level or the Series B level even if there is less capital available in other markets. But you can see that there is a big difference.

1b) One side note: also, if I remove startups who have founders with pedigree, then SF doesn’t punch above its weight and proportionally stays the same at each stage.

2) International companies outside of the US & Canada have a much harder time raising money.

You can see that across-the-board, my international companies have had really had a tough time getting to the Series A or Series B level.

And again, I attribute this to less access to knowledge about scaling, less access to capital, and less access to talent that has scaled businesses before. One potential wildcard explanation for this lack of success is that the US & Canada have pretty established customer acquisition channels. But, that isn’t the case everywhere globally, so it may also be that customer acquisition makes marketing and sales in the US & Canada just faster and that other international companies just need more time to make headway.

3) Companies based outside of the SF Bay Area that have been successful have spent significant time in the Bay Area

The last interesting thing I would say here is that if you look at the Series B companies, anecdotally I can tell you that all of those founders have cultivated lots of relationships here in the SF Bay Area to get scaling knowledge and access to capital.

Takeaways:

I don’t think you need to be in the San Francisco Bay Area to start a company. In fact, I actually think that since your money goes so much further elsewhere and knowledge is commoditized regarding starting a business. As an early stage founder, you really should just focus on product-market fit wherever you feel is best for you to live.

BUT! If you want to start scaling a business – call it at the Series A level and beyond – that’s when you really need to start having connections ideally to the SF Bay Area to raise money from and have a network / learn from and potentially even a pool of people to hire.

If you are starting a business outside of the Bay Area and want to build a unicorn business, in today’s global economy, it is significantly helpful for you to start building from connections on day 1 to the SF Bay Area.

One of the more taboo topics in “Startupland” is around having a family while starting a business. When I was about to have my first child while working on my company LaunchBit, I was catching up with a friend of mine who was also an angel investor in my business.

And then he asked me, “How do you think about balancing your company with a young child?”

Since then, it’s a question I’ve batted around for years. Is this an appropriate question? Is it even a good question? And what is even an answer to this question?

To be clear, my friend didn’t mean any malice by it nor was he trying to use my answer as a piece of information in making a decision about investing — he was already an investor. He was just legitimately curious. But of course, the immediate counter question that comes to mind (and that I articulated out loud) is, “Would you have asked me that question if I were a male founder / CEO?”

We all know that he wouldn’t have.

For as long as I’ve been running my own company — first at LaunchBit and now at Hustle Fund — I have not often engaged in conversations about family in business meetings / business settings. When other people talk about their kids, I usually just kinda smile and nod. In contrast, my business partner at Hustle Fund Eric often talks about his family and his minivan. He shares photos of his children with our investors in our monthly reports regularly. I don’t think think most of our investors even know that I have children. There is an unspoken looming fear that many female entrepreneurs with children have — that their abilities and dedication as a professional will be judged and looked down upon because they have children. This is because there is a notion held by some people in the ecosystem that having a startup while having children puts you at a disadvantage and shows a lack of dedication. Obviously, not everyone holds this belief, but there is no upside as a woman to sharing that you have children while running a startup. And so for so long, I’ve just generally kept quiet / private about the whole matter.

And I’m not the only woman to do this. Countless female founders of mine over the years have asked me for advice and guidance on managing a family while starting a company but have also asked me to keep these questions on the down low or even their plans to start a family on the down low. I’ve become a confidante of sorts because I’m a female founder with a family in this taboo world.

However, after mulling on this for a few years, I think the exact opposite needs to happen. Everyone would benefit by sharing advice on tips for handling parenting while running a startup. And, so I’ve decided to write this post on how I’ve managed to balance parenting while running 2 startups (had kid #1 while running a product startup and had kid #2 while starting a VC fund a couple years ago).

Before I had kids, I had in my mind an idyllic notion of parenting. I thought I would swaddle my newborn in cloth diapers, feed breast milk for a year, and follow every other piece of advice from “ideal mother” websites. But then, reality quickly set in – in having my first child while running my adtech company. The idea of spending an extra 30s putting on a cloth diaper at 2 in the morning in a half dazed stage all of a sudden seemed less exciting — my stance on parenting immediately changed when I became a parent — I just wanted to make sure my kid stayed alive and healthy!

The reality check

On one hand, there is truth to why running a startup and raising children isn’t easy. Many people will say that it’s because children take up a lot of time and attention. Other people say it’s because they increase your financial burden. Both are true but IMO not the biggest issues namely because people are incredibly resilient to constraints — both time and money constraints.

For example, before I had children, I thought I was quite efficient with my time. Post-children, in looking back, I’m actually 3x+ more efficient with time now. I never thought I could eke out so much more efficiency. You can ALWAYS become more efficient with more constraints.

Playing Bejeweled is something I used to do but don’t anymore…

So, the biggest challenge isn’t additional constraints, because resilient people make things work and make them work better. I actually think the biggest challenge is that there are just a lot more variables that are out of your control.

For example, your kid gets sick and can’t go to school; that’s out of your control. Your kid wakes up every two hours; you can’t control that either. So how do you deal with last-minute situations? How do you impromptu handle situations you didn’t expect?

So, here are some key things I’ve learned while leveraging my time as an entrepreneur parent:

You need support. Don’t do it alone.

You need to say no and leverage time.

You need to “let go.”

Support

It really does take a village to raise children, and I’ve leaned on tons of people for support from the beginning through now. I think people are often afraid to do so, but I think it makes life a lot easier.

During the first few weeks of motherhood, folks showed up with home cooked food or bought meals / meal gift certificates for me and my husband. Beyond the warmth of love and generosity this brought us, such a little act made a big, practical difference in my day. I could then put my energy towards thinking about my business, focusing on my kid, and even some personal recovery time, instead of worrying about what we were going to eat for dinner. On the flip side, this is probably the easiest, best gift you can get a new parent — meals.

My support network helped me balance time as I became a first and then later second time mom while being an entrepreneur. When my kids were still very young, friends and relatives babysat while I went to networking events, to work, or to sleep when I desperately needed a nap. For example, when I was fundraising for Hustle Fund in 2017, there was a networking event on a Saturday in San Francisco, and my husband was out of town. For the 2-3 hours that I was there, I left my baby with my friends who lived in the Mission. As an entrepreneur, at work, you ask for the moon from your business partners and potential clients all the time. But we don’t often do that with people we’re closest with. Why not?

My husband holds down the fort a lot, especially when I travel for work or have late meetings or events. And my parents have spent so much time with my kids when they have no school (and in the very beginning when they couldn’t go to daycare), I can’t imagine accomplishing both startups without them or my extended support network.

Pride is one thing you really can’t afford when launching into the role of a entrepreneur-parent.

Saying no & leveraging time

As a parent and entrepreneur, I need to leverage my time, and I need as much of my 9am-5pm working block to be free to think / write.

To achieve this, unfortunately, this means I end up saying “no” to a lot and moving things to more efficient channels whenever I can.

For example, people ask other people for coffee meetings a LOT! Usually without any purpose. I used to do these coffee meetings a lot in my 20s. But, now, I often say “no” to coffee meetings. Critics of this strategy may argue, “Well, I’ve built my best connections through coffee meetings.” And I can agree coffee meetings are great to a) re-build or strengthen rapport with someone you already know / want to catch up with a friend OR b) meet with someone new and build rapport with LOTs of coffee meetings with him/her. But when I look back, the vast majority of my coffee meetings in my 20s have been one and done, and for those people, that one coffee meeting isn’t enough to end up doing business or hang out socially in most cases. (there are some exceptions but largely true of the coffee meetings I’ve done over the years)

Instead, I prefer to stick with email for quick communication and if necessary, move to a phone meeting while commuting. In fact, I set up my Calendly so that bookable times are primarily during my commute at the beginning and end of the day. I end up having a lot of meetings while walking, skateboarding, kick scootering or driving.

For further “networking”, in lieu of a 1:1 coffee meeting, I like to do group drinks / lunch or hangouts outside of my 9-5 working block. So if there are a handful of people you want to re-build rapport with or want to get to know, it’s a lot more efficient to group everyone together. And they’re busy too, so they want to make the most of their limited time too.

This means that when I get to work at 9:00am, I’ve already done a few calls / networking, so most of my 9-5pm day is slated for “thinking work”. I might have a couple of additional meetings during that block where I need to take notes and be fully thoughtful, but I like to have — as much as possible — a whole day to only do thinking and writing work.

The opposite of this schedule is what I had when I was working at Google in my 20s. I had back-to-back meetings all day, and then when I got home, I would, in a tired way, try to think and write. In retrospect, if I were to set up my schedule all over again, I would have skipped many of those meetings, asked people to do most work / coordination over email, and done calls while commuting to free up most of the day.

Exercise

As an aside, exercise is really important to me, and combining work time with exercise (walking, jogging, skateboarding, kick-scootering, etc.) allows me to eke out additional productivity. I don’t believe in multitasking for most things – I think multitasking makes it challenging to really focus and be present. But I do think that exercise and talking-work goes well together, and this type of multitasking actually is more productive.

I read Christopher McDougall’s Born to Run (excellent book) and learned that our ancestors used to hunt animals by basically jogging a marathon everyday! Since then, I’ve been trying to increase my miles–some days I walk eight miles–and multitasking with phone meetings helps with this goal, too. I’ve also heard that walking is more conducive to thinking than sitting — but who knows?

In addition, I often use voice-to-type to “write” emails on my phone, especially during commutes. Whether walking, jogging, or scootering with my kids, I can still “talk” to do writing work.

Emails

Lastly, everyone gets TONs of email these days, and email management is a big chunk of work in itself. It’s really important to me to keep my 9am-5pm working block mostly free — I don’t want to be spending most of that time in email. With the exception of a few emails that need immediate response, I work on email on the Caltrain on the days that I go up to San Francisco or at night after dinner.

I also recommend SaneBox, Superhuman, and Gmail smart responses to streamline emails and Calendly to streamline calls.

I use SaneBox to filter a lot of emails including subscription emails, emails from people I’ve never met, etc.

I use Superhuman for templated responses so that I can tell everyone the same thing over and over again. For example, if I need to move a conversation to a call, I send the same templated response with just a couple of keystrokes, and people can pick their own time to chat (during commute hours) through my Calendly calendar management. I also use Superhuman for offline email processing – so for example, if I’m commuting on the Caltrain to San Francisco, I can plough through all my emails offline quickly.

Re-scope responsibilities and letting go

Outside of work, the time it takes to complete simple chores adds up and eats away time and energy you could be spending either working or with your kids. Since working on a startup means having a budget, my husband and I have re-scoped and re-prioritized our chores to make them as manageable as possible.

Laundry. To save time, we don’t fold laundry. We just don’t. I know – that sounds blasphemous. That’s a tradeoff that we’ve made. We each have a laundry basket to keep clean clothes separate, and we wash each person’s laundry in their own load. I also streamline my clothing options by wearing a @HustleFundVC shirt and jeans almost every weekday. I understand that not everyone wants to keep his/her clothes in a laundry basket or wear the same outfit over and over, but I can tell you that it saves me a lot of time. Sometimes you just have to let go and figure out what is really important to you.

Food. Each week, my husband and I each cook one simple dish, usually on the weekend. One night, we’ll order cheap delivery, one night we’ll end up eating at someone’s house, and one night we’ll pop a frozen pizza in the oven. Leftovers carry us through the rest of the week. Keeping our meals simple means neither of us has to fret over grocery store runs or recipes.

Dropoff and pickup of kids. We only have one car, so we each take a day to do both dropoffs and pickups. We are fortunate to have managed to get their schools to be close to our work and home, so our commute, in general, is not that long. (A miracle in the Bay Area where there is tons of traffic) .

When my kids are not in the car, this is when I do my car calls so that the drive time is not wasted. When the kids are in the car, it’s actually a good time to chat with our kids. Conversations don’t just have to be at home at the dinner table. They can be in the car too. Since we only have one car, on other days, I will sometimes combine exercise while the kids are in a double stroller or while we’re kick-scootering together and will take calls when the stroller is empty.

Double stroller + skateboard combination day

Contractors. People have often asked me if I have a nanny or if I hire a company to clean our place. I’m not averse to this, and in general, I believe in comparative advantage. Meaning — if someone else is way better than you at something, for the right price, you should hire help. This is how you’d run your business; and, this is how you should run your home.

In our case, both of my kids go to school, so a full-time or even part-time nanny wouldn’t be helpful because he/she would have no children to watch during the day. And by setting up the above the systems, things like laundry actually don’t take more than a few minutes — a chore that could take hours you can shortcut by basically not caring. So should I pay someone for something that I fundamentally don’t care about is the question? Not sure.

I also make my kids — as young as they are (both under 6) — do chores. In the beginning, it’s not done well, but at this point, they are actually quite good at cleaning and feeding themselves.

But I do think you should pay for things that you do care a lot about and will take a long time (such as this blog post!). That’s how you can get further leverage on your time.

To summarize

Running a business and being a parent each requires a lot more juggling than without children. But, it also forces you to be pretty dam* efficient that you could possibly imagine.

To summarize, the biggest way to leverage time with a low budget is to a) ask for help from your community (family, friends, and even your own kids); b) prioritize thinking work and figure out how to get rid of everything else; combine with exercise, and c) reduce how much you care about daily chores.

My business partner Eric at Hustle Fund is appalled by the fact that I don’t fold my clothes, so these exact strategies are not for everyone, but I do think with some creative juggling, you can eke out a lot of additional efficiencies to make parenting and entrepreneurship work without going crazy.

Special thanks to my editor Caitlin for pulling the first draft of this together. Also, the stock photo above isn’t a photo of my kids, but they are cute.

“Contrarian perspective here – it’s ok to *not* meet a founder in person before deciding to invest.”

This set off a tweet firestorm — mostly with people telling me in some form or fashion that I was wrong. (Side note: what I love about the VC industry is that people tend to have incredibly strong opinions based on limited or no data :) )

It’s interesting — at this point, I’ve been investing in early stage startups for almost 5 years. And, I still have a lot to learn. But I’ve also personally interviewed 1000+ early stage startup teams.

Most of these teams in person.

And after looking at all this data about interviewing, I believe that it actually doesn’t really matter *for me* whether I interview teams in-person or remotely. Let’s dissect this a bit:

First, why should you interview startup teams in person?

1) I think cultural and historical business norms would say that you should always try to meet people in person and try to build rapport in person to win a deal.

While I don’t think anyone has great proof on this, intuitively, I believe this is true. What better way to win a deal than to fly to a founder and just show up and say, “Hey, I want to invest”.

So for investors playing in highly competitive spaces, this makes a ton of sense. E.g. investors going after a hot series B deal. Or for investors chasing after founders who came from Facebook and MIT who are building the next scooter company that utilizes AI. Building rapport is really important to winning hot deals.

For me, most of my deals are not hot when I invest. Hah. Often these companies go on to be hot later. But since I’m first check into companies when they basically have nothing, usually it’s just me and the founder’s mom who are investing. Writing the check is in itself the rapport-building activity.

2) You can assess founders better in person.

I also believe you can assess founders better when speaking with them in person. You can detect when there is co-founder tension / drama / something weird. You can detect when a founder is stretching the truth. All kinds of stuff.

I know this because I’m a super blunt / direct person. And, I’ve often called out things to founders directly. For example, there have been many teams over the years where I’ve noticed tension in a meeting between the co-founders. I’ve often pulled founders aside afterwards and mentioned my observations as such. e.g. “Hey, it seems like there’s some weird tension between you — are you having a lot of miscommunication?” And every single time, founders have broken down and admitted that they’ve been having some problems. You can definitely detect co-founder issues in an in-person meeting.

So given these huge benefits, why wouldn’t you meet a team in person? A bunch of reasons…

1) Unconscious biases.

It’s amazing how a team that is great at pitching can really “fool” you. There have been so many meetings I’ve taken over the years where you walk away from the meeting feeling really pumped and believing that the founders are amazing. And you think, “These are great founders!”

And then, I look back at my notes 24 hours later and re-read everything they’ve done or not done in the last few months, and you think, “Oh, this just sounds ok – they’ve only sorta achieved some things.”

Charismatic people can really fool you. Having charisma is a great trait, just in general. But, it can mask actual execution.

Moreover, charisma is cultural. What we find inspiring in a leader in the US is very different from what other people in other places of the world find inspiring. So, we have unconscious biases around what makes a charismatic leader. Extroverts, for example, in the US have a huge advantage. We generally think of extroverts as highly charismatic people. But extroverts are not actually any better leaders than introverts. There are plenty of examples of successful introverts who manage to inspired large groups of people towards a common goal. So we let our unconscious biases get in the way in assessing things like leadership because of the way our culture is set up.

One of my learnings over the years in venture is that it’s really important – as much as possible – to be objective. I try to assess what a team has actually achieved. Or what they are actually doing. But very often, meeting people in person detracts from assessing this, because some founders are much better at selling the dream and others are much worse.

There’s a well known top female VC who works at a very well known VC fund, and she was telling me a few years ago that one day her partnership heard 2 pitches. One of the pitches was by a woman who matter-of-factly just talked about numbers and growth and how she could build a big company. Another pitch was by a man who sold the dream and hadn’t done much of anything. After both meetings, the rest of her partnership talked about how they could really relate and build rapport with the male founder who was quite the visionary. This top female VC, however, realized that, although she was more excited about the male founder’s pitch, when she objectively thought about what he had accomplished, she realized it wasn’t much. And that the female founder had knocked it out of the park although her storytelling wasn’t as amazing. This story is a true story and this happens all the time in venture.

In the venture community today, we reward “visionaries” much more than executors. And a big reason for this is that we make investment decisions based on pitches rather than on execution (aka working) in our decision-making. This is a big problem and this is precisely what I want to change at Hustle Fund (though it takes baby steps).

The last piece about unconscious biases is that sometimes what we see in-person scares away traditional VCs. Such as pregnant women. Being a pregnant woman and pitching investors is NOT a recipe for success to raise money. Although there are plenty of successful female CEOs who have children while running their respective startups, it’s still not a positive sign to most VCs. This is a shame and something that is only noticeable / an issue when pitching in person.

2) Meeting teams in person limits your deal flow.

At the earliest stages, it’s important to see a lot of dealflow. If you are only doing meetings in person, it means that:

Companies can only be located in your geography

You need to spend a lot of money and time to fly to other places to see companies

You need to spend a lot of money to fly companies to see you.

If you’re a series B firm, all 3 of these can be fine limitations. You presumably have enough management fees to spend money on travel, and presumably, you don’t need to be seeing tons of companies in order to do great deals. But if you are at the earliest stages — such as a pre-seed fund like ours — you need to be seeing lots of deals and generally don’t have the budget to either do a lot of traveling or to fly companies to you.

And at the pre-seed level seeing lots of top-of-funnel deals is critical!

So, meeting teams in person is a tough strategy for small firms like ours — for both time / money reasons.

3) Technology is good-enough for remote meetings these days.

Technology is actually quite good these days. I think 10 years ago, vetting people through video conference might have been rough. But, today, Zoom.us, for example, is an amazing product for doing video interviews. You can see a lot with strong connectivity — including founder tension — and you can really feel like you’re in the room with the founder.

4) Meeting people in person is inefficient.

I don’t want to waste founders’ time and my time. The priority activity for them is in running their business. So for the most part, driving all around the Bay Area (in traffic!) is not a value-add activity for anyone. If we happen to be in the same place at the same time, that’s great — such as a conference / event / co-working space, but for the most part, commutes are a bear that I don’t think anyone should have to put up with if given the choice.

5) Lastly and most importantly, if you construct your portfolio in a certain way, it’s actually ok to miss things in a virtual interview.

After investing in hundreds of startups, I genuinely believe that it is much better to invest based on execution rather than to try to assess accurately based on talking. But, the entire industry is largely based on making investment decisions based on talking. This is a grave mistake, in my opinion.

Here’s an analogy in the job market — in the old days, you would interview a bunch of candidates. And then you would pick someone to hire largely based on talking. But as it would turn out — people who are great at selling themselves in the interview process are not necessarily the best performing hires! Business people have figured this out, and so these days, at so many companies, you no longer just talk in a job interview. Hiring teams now try to assess in other ways — through projects / short term contracts / tests / etc. In other words, execution-based tests are now used much more commonly to better assess hires.

In VC, the right analogy would be — why don’t we make a small bet for seemingly promising companies? And then try to assess based on execution whether or not to write a much larger check. (On the flip side, startups can assess us/me, to see if I’m living up to standards as an investor.) And as performers perform, let’s continue to do this. This seems like the much better way to assess performance — by actually assessing performance itself rather than talking.

For this reason, this is why I think it’s actually ok to miss some things in interviewing founders for a potential investment — because I care much more about how a team performs than how they talk & look.

Obviously both are important for a successful marketplace! But, if you want to build a really BIG marketplace, here are some observations from over the years.

1) Unlocking large amounts of supply matters A LOT!

This is a bit unintuitive. Most people who set out to build a marketplace think that if you can get people to pay for something (the demand side), then you’re all set. I’ll argue that it’s certainly important to test the demand side but it’s almost more important to test how hard it is to get supply.

From my experience in growing an ad network, it is possible to have lots of demand but not enough supply! This is actually a very common phenomenon. Case in point, most email newsletter companies have an easy time selling out their ad slots, but it’s incredibly hard to continue growing an email newsletter at a fast clip. The way that a lot of email newsletter companies solve for this problem is by introducing new lists with the same audience. E.g. you can receive the daily news digest and also the daily jobs email. This gives them twice as much supply with the same audience.

2) If you are aggregating supply, the key is to unlock new supply

One of the big areas where I see marketplaces fail is by going after an existing market and trying to amass the same supply that already exists. So for example, a marketplace for salons or a marketplace for wedding venues or a marketplace for co-working spaces. These marketplaces are all amassing existing salons or existing wedding venues or existing co-working spaces. These are existing places that consumers could ordinarily find themselves and pay for directly. You are literally just moving supply around and not growing it. The issue with doing this is that this existing supply already has certain expectations for payment, because they are already making money for this service or asset that they provide. This then makes it hard to be a middle(wo)man and take a cut in between. You are competing with a strong alternative — to be found directly.

The better way to aggregate supply is unlock new unique supply. Airbnb is a great example of this. People were not already using their extra bedroom as a hotel room or their couch as a bed. They don’t have the same expectations around making a ton of money unlike the Holiday Inn. Airbnb has effectively brought a ton of new “hotel room supply” to the market that didn’t exist before. They were not try to resell existing rooms in existing hotels. Uber and Lyft are equally good examples of doing this in the taxi market. They brought into the taxi market new “cab supply” that didn’t exist before, and these drivers don’t have the same expectations for monetization as existing taxi drivers.

Ultimately, unlocking new supply drives demand. If I can stay on someone’s couch next to the Moscone to attend a conference for 50% of what I’d pay for a room at the Holiday Inn, I’d do it. You are reducing prices for the end user by unlocking new supply, and this drives demand.

So going back to the original examples of marketplaces for salons or wedding venues, etc, can you get clever / creative in creating new supply? Can you turn new people who are not in the salon business into a salon owner? In many cases, doing this might just be too high of a cost and not possible, but in some cases, this approach may be a good strategy. A good example of this is Wonderschool. Wonderschool is turning people into new daycare owners — they are not amassing a network of existing daycares but rather unlocking and creating new ones to add to their network. So think about unlocking new supply rather than moving existing supply around.

3) The unit economics need to work in the long run at scale

Once you initially test both supply and demand, there’s going to be a constant tension between both sides. Sometimes you’ll be supply constrained. Sometimes demand constrained. Often, it may not be clear if the unit economics will work out while you’re building this up.

In fact, ridesharing companies often get a lot of flack from the public, because they are not profitable yet. But, the holy grail for them is autonomous cars. Once these become mainstream, they will have access to infinite supply at a low cost. So while the short-term numbers may be questionable, the long-term future of these companies seems very promising.

Similarly, you’ll need to think about what your long term control over supply will be. Most marketplaces that are successful have a stronghold on at least a good portion of their supply to help with pricing pressures. Successful ad networks are a great example of this — Google may run a large ad network across many properties they don’t own, but they also own a lot of their own properties including Google search and YouTube. Likewise, although Airbnb doesn’t own properties today, it’s rumored they are going into real estate. So once you get some footing on your marketplace, the next question is how can you think about controlling your future by having access to or creating at least a good portion of your supply?

4) What should I look for in amassing unique supply?

If I were to build a large marketplace today by amassing supply, I would start by looking around at what is currently wasted (space / time / assets). Then, I’d think about how this wasted stuff might be cleverly transformed into something else that consumers and businesses currently spend a lot of money for.

Summarizing all of this, to make a marketplace fly, you need to cleverly come up with a LOT of unique supply (obv there has to be demand). 1) Turn something else into supply where people don’t have high monetization expectations (Airbnb, Uber, Lyft). And/or 2) eventually you own it or part of it (e.g. scooters / Google search).

At Hustle Fund, we talk a lot about speed of execution. Part of this is grit and founder hustle. But what most people don’t realize is that speed is also baked into the business model itself.

For example, one of the things that people don’t realize is how much sales cycles and payback periods matter. As a concrete example, fast growth direct-to-consumer companies are now able to go from $0 to $1m revenue within a month or two with just < $25k in ad spend. This is incredibly fast — unprecedented and very low cost.

How is this possible? All because of fast sales cycles. Let’s dive in:

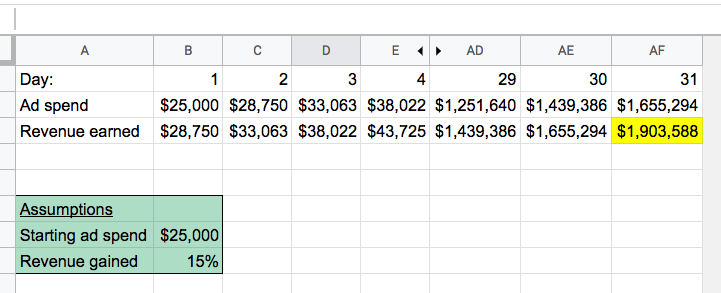

Let’s start with a simple example. Suppose the following:

We start with $25k in ad spend on day 1

As soon as people click on our ad, they buy immediately and we get that revenue immediately

For every $1 we spend on our ads, we make an average $1.15 in revenue

We pour everything back into ads the next day

You can see that within a month, we are at an almost $2m revenue generated with just initial ad spend of $25k! This is crazy. You can raise a small pre-seed tranche and get to Series B benchmarks within a month.

Now, in practice, the scenario I’ve outlined is near impossible. Namely, most of the time, your ad spend is not this effective on day 1 and often requires iterations and testing. Moreover, it often takes some time to clear with your payments provider even if you generate revenue right after someone clicks your ad.

But this scenario is actually not that far off from what many of the direct-to-consumer incubators are achieving.

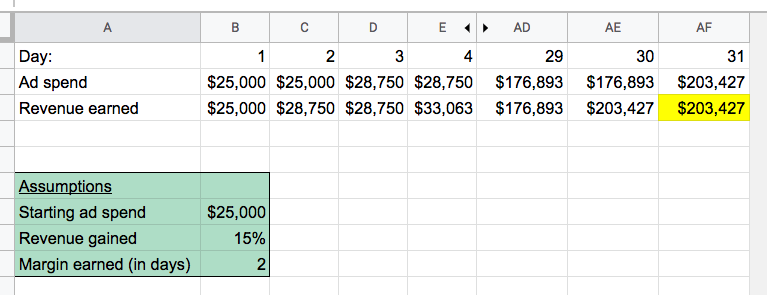

Ok, let’s add some delay to make this a bit more realistic. Let’s suppose:

We start with $25k in ad spend on day 1

As soon as people click on our ad, we do get our initial ad spend back immediately but we don’t make any profit until the even numbered days

For every $1 we spend on our ads, we average $1.15 in revenue (on the even days)

We pour everything back into ads each day

This is a contrived example (profit only on even numbered days?? weird.), but you can see in this example, we went from a near $2m revenue generated at the end of the month to just a $200k revenue generated, even though the delay in our profit is not that long. Not only that, we are making about half the profit as before, but our revenue generated has now dropped by nearly 10x. Why? Because time is a compounding factor.

So when investors are concerned about sales cycles and payback times, this is what they mean. Regardless of whether you are using ads to get customers, if you calculate this out, you can see how just small affects in sales cycles / payback periods hurt you big time. The other thing is that as an entrepreneur, you’re working just as hard in the first scenario as in this one, but your sales are affected 10x.

Both of these examples are still a bit contrived, because as I mentioned above, you usually don’t know if your ads — or any of your customer acquisition channels – are working (they probably aren’t) on day 1.

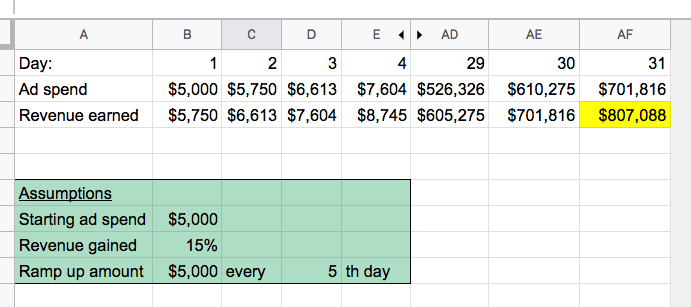

So now let’s assume that you don’t start with $25k in ad spend. Let’s start with $5k. Suppose the following:

We start with $5k in ad spend

As soon as people click on our ad, they buy immediately and we get that revenue immediately

For every $1 we spend on our ads, we make $1.15 in revenue

We pour everything back into ads the next day

We add an additional $5k in ad spend every 5th day

You can see that with this example, we can get to near $1m revenue generated by the end of the month ($800k+). In this case, we end up spending a bit more on ads, but this is a more gradual (and realistic) approach to ramping up ad spend. Again, in this example, because we make the $1.15 for every $1 immediately, you can see that this helps us achieve greater revenue than in the prior example.

In your own business, how can you decrease your sales cycle + payback period by even just 10%? How can you increase your margins by even just 5%? These all add up significantly as you can see over short periods of time.

The tl;dr is never underestimate the value of time in making money.

Here are some things that I think will be big in 2019:

1) Furthering vocational education

I think traditionally, a lot of investors have been shy to invest in education. In US, let’s be honest — we don’t really care about education! Here’s a good post that my friend Avichal Garg wrote on the education landscape several years ago which I think still applies today in the US.

But the tide is changing a bit. Specifically, what we’re seeing in the US is massive student debt. And new college graduates are not able to get a job or a high paying job. For so many people in the US, if you are not majoring in a STEM subject, it probably does not make sense anymore to go to college. Period. The economics of college are just terrible.

So while we don’t care about education in the US, we do care about business and return on investment! And it does make sense now to provide education of “useful” topics for the workplace — for a job, for livelihood. This is why we see the rise of Lambda School which ties your livelihood outcomes to your cost of education. And there are many other schools that are cropping up such as Make School and Kenzie Academy (we are investors at Hustle Fund) that are trying to teach useful topics that you can actually use and are willing to pay for, because you can use those skills to make money.

I think we will see a lot of new businesses stemming off of this trend.

We’ll certainly see more schools — both in-person and online covering more topics. Everything from coding to digital marketing to sales to even entrepreneurship. But also vocational categories as well. Can you teach medical skills or plumbing skills using VR headsets remotely?

Additionally, I think there will be businesses stemming off of these. Lots of new ways to loan money to students. New ways to provide socialization and networking for remote students. New real estate opportunities for these students.

2) Improving commutes

Commutes are terrible! (and a big waste of time). This year, we will see a lot of businesses built around making your commute better. Commutes can get better in two ways: A) By actually reducing your door-to-door time and B) by making the experience while commuting better. We’ll see opportunities in both.

A) There will be new ways of commuting in less time.

This is really what the rise of Bird and Lime is all about. When it’s faster and cheaper to go from say SOMA to the Financial District of San Francisco by scooter vs car AND is accessible to everyone, people will do it. In contrast, not everyone can ride a bicycle or a skateboard (e.g. more expensive, need balance or skills – not accessible to all)

But scooters really only work in warm-ish places where there are bike lanes / wide enough roads. E.g. places where it snows / places that don’t have bike lanes won’t be great markets in the long run. So there’s an opportunity to come up with a mode of transportation and model that can withstand weather / lack of bike lanes. My guess is that we will just see further advancement of ridesharing combined with autonomous vehicles. An early version of this might be effectively new autonomous bus lines that just go up and down streets continuously. This is already starting to happen in some cities.

B) As people drive less, they will have more time during their commute

This is a big opportunity for people to do more work, shop, and play more too. For example, we’ll likely continue to see growth in podcasts and tools for podcasts this year. Spotify made clear that they believe in this opportunity by announcing two acquisitions in podcasting this week.

But we might also see the emergence of new commuting activities. Such as new commerce models. In Asia, for example, lots of people shop while waiting for public transportation like this:

We may even see new fitness activities. Peloton allows you to exercise at home in a social way. Can you do this on the road? Can you take a stretch class in an Uber? Can you run from Zombies or have a coach yelling in your ear while you run to work?

A general trend we’ve been seeing over the years is the ability to entertain yourself in a retail location, and later this entertainment was brought into the home and then later yet, taken anywhere, especially while commuting. For example:

Before, you shopped at the mall -> Later you shopped on your Desktop browser at home -> Now shop on your mobile device while commuting

Before, you played video games at the mall -> Played video games on your Desktop -> Now play video games on your phone while commuting

Before, you watched shows at the theater -> Watched shows at home -> Now, you watch shows on your phone while commuting

Before, you went to the gym to workout -> Now, you work out at home -> Later, will you work out while commuting?

Maybe. I can’t predict the future, but I can tell you that people will have more time with their commutes.

3) Furthering entrepreneurship

When I grew up in the Silicon Valley in the 1990s, entrepreneurship was a ridiculous idea. You were a maverick if you were an entrepreneur. This is no longer the case. You’re pretty mainstream if you’re an entrepreneur today. Even outside of Silicon Valley, so many people have side businesses.

I think entrepreneurship as a category has gotten so big that it needs to be segmented. There are fast growth tech startups — these are the ones that VCs like to find and back. There are brick and mortar retail businesses. Like cafes and restaurants. And there’s a new emerging but fast growing category that I call the “micropreneur”. Micropreneurs are < 10 person companies that are supported largely by existing web platforms and online distribution. With just a handful of people, these founders can generate as much as $100k-$1m per employee because they can leverage a lot of existing infrastructure — online payments, website builders or online store platforms, and even easy-to-use “pseudo-developer tools” such as Zapier. Micropreneurs are fueled by the rise in platforms that help people get a business off the ground — such as Shopify or Webflow (we are investors at Hustle Fund) or Stripe or Udemy. Or even YouTube and Instagram! They are often bootstrapped and often start as side businesses that sometimes become full-time businesses. And unlike tech unicorns, there are tons and tons of them.

I think 2019 is the year where we see products, platforms, and content for the micropreneur.

Entrepreneurship education platforms (could be schools / bootcamps / etc of sorts) especially in areas of customer acquisition

Loans / financial solutions to provide non-VC funding for these businesses

Unique platforms and tools that can make it easy to start a “scalable” micro business

networking platforms and clubs (like a YPO for this segment)

In general, I believe that if you can help people make more money, that is the easiest sale, and microentrepreneurs are hungry to buy things that will fuel their businesses that are already doing well.

4) Crypto tools and crypto platforms

Although we’re in the bear markets with crypto, I am bullish on the long term use of cryptocurrency. Why? Fiat works fine in many places. But, I think what we are increasingly seeing is monopolistic behavior on the internet.

I applaud CEO of CloudFlare Matthew Prince for writing this post a couple of years ago about free speech on the internet. In this post, he talks about how CloudFlare came to the conclusion they should terminate The Daily Stormer as a client. It was a difficult decision, not because he agreed with the Daily Stormer’s ideology, but rather because he didn’t believe that internet companies should be policing the internet for people who hold opposing ideologies.

But this is happening. We’ve seen a lot of large internet companies terminate relationships with people they don’t agree with. As a response to that, I believe we’ll see new sites crop up to try to bring back a “free internet”. Payments are usually at the front of new waves of trends, so I suspect, we’ll see decentralized payment options pop up as a response to PayPal / Stripe / et al kicking people off their services. Technology tends to start off with illicit use cases (such as the VHS tape used for pornography) but then ends up becoming mainstream.

In order for people to pay each other with cryptocurrency, we need reliable and easy-to-use infrastructure that mainstream consumers can use. This includes digital wallets for storing cryptocurrency, easy-to-use exchanges for moving money from currencies to fiat, accounting solutions for cryptocurrency, etc. Entrepreneurs are currently building in all of these areas, and I’m bullish on innovation in all of these.

In this space – I think the winners will have to be incredible product designers who can build great user experiences. 5) Verticalization of B2B SaaS

In North America, B2B horizontal SaaS business ideas are largely saturated. Not 100%, of course, but for the most part, we have marketing software, sales software, HR software, customer service software, and communications software that largely works. Some of these tools may be clunky archaic experiences, but they are here to stay — at least for a while, in my opinion.

So I think the B2B SaaS opportunities that people will focus on are verticalized use cases. E.g. Marketo for XYZ industry. Software built around particular sales cycles and workflows for industries like real estate, construction, farming, retail, etc. We already see this happening, but I think there will be a lot more of these types of businesses built around verticals in 2019.

I could be completely wrong on any and all of these predictions! And, even if I’m right, outside of these 5 categories, there will be, of course, many more businesses built.

What startup opportunities do you think will be big in 2019?

A couple months ago, we announced that we finished fundraising for fund 1 of Hustle Fund. Hustle Fund is my new venture capital firm, and our fund 1 is an $11.5M fund dedicated to investing in pre-seed software startups. Eric, Shiyan, and I could not be more grateful to our investors for their support and to so many of our friends and family who helped us with this process!

I’ve written before about what it’s like to start a new venture capital fund. But, a lot of people have asked me about how we actually raised it. Surprise surprise – we ran our fundraising process using all the fundraising tips I give away on this blog!

First some context

I need to spend a minute explaining a bit about venture capital (VC) structures. VCs raise money from other investors called limited partners (LPs). These investors can be individuals / family offices / corporations / institutional funds that invest in VC funds.

Here’s how we raised our fund (and some learnings):

1) We talked with a dozen fund managers before starting

If you are considering raising a VC fund, I would highly recommend talking with a TON of new fund managers before jumping in to a) make sure this is what you want to do and b) get tips and advice. The single-biggest tip that I heard over and over from my peers was that they felt that they had spent a lot of time courting large institutional fund investors when they should have spent more time trying to find family offices and individuals and corporates to pitch. We took this advice to heart and ended up only meeting about 10 institutional investors once or twice to build relationships with them – potentially for down the road.

In the startup-fundraise world, this is analogous to raising from angels vs. VCs. If you’re super early, meeting with angels is likely going to be the more successful fundraising path. VCs will take meetings with you, but you want to make sure you are not spending too much time with people who will most likely not be investing right now. That being said, it can be good to build relationships for down the road. This is a time tradeoff that every founder — both product founders and new fund managers — have to make.

2) We sized up motivations

This leads me to my next point. It’s important to size up an investor’s motivations – and this applies when fundraising for a product startup as well. When you’re meeting with an investor, try to understand why he/she is investing — just in general.

There are many many reasons why someone wants to invest money in companies:

To make money

To not lose money

To take large risk but potentially very high return

To get promoted / move up the professional ladder by making a good investment

For fame and glory and bragging rights

To learn about a business or industry

To network with other investors or the founding team

etc..

Points #1-4 seem similar but they are actually quite different. Some people are motivated by making money. Others are motivated by wealth preservation (to not lose money). An example of this is that many large institutional fund-of-funds manage retirement plans. Their goal is to preserve the wealth of the everyday hardworking people who entrusted their savings in them. Think about it – if you are working for SF MUNI and put your hard saved earnings from your salary into your company’s retirement plan, the last thing you want to hear is that your retirement plan lost all your money by investing in some dumbass new fund manager who invested in dogsh*t startups! Most retirement plans will not be investing in unproven first time fund managers.

Others don’t mind losing money if there’s the potential to make above and beyond a TON of money. E.g. you invest $10k and it has a 95% probability of being entirely lost but there’s a 5% chance that it could make $1m.

Then, there are lots of non-ROI reasons to invest. To learn about an industry or a new technology. To brag to friends. To network with other investors or the founders. Etc. These are all equally great reasons to invest.

Most people have a blend of reasons, but it’s important to figure out what that blend is.

In our first meetings with all the investors we met with, we tried to assess what motivated each person we spoke with to get a sense of whether an investor would likely be a good fit. (More on this later)

3) We prioritized speed over dollars

Our focus for this raise was on speed. According to Preqin, in 2016, it took first time fund managers an average of 17 months to close a first fund. For us, we decided that we really wanted to raise our fund in less than a year (and ultimately closed in 10 months). So if it meant raising only $5-10m vs $10m-$20m in twice the time, we wanted to opt for less money at a faster pace. This essentially dictated our strategy to raise primarily from individuals, because they can make decisions quickly.

The main reason why speed mattered to us is that per SEC rules, we could not market our fund while we were fundraising. As marketers, we wanted to start actively marketing Hustle Fund as soon as possible.

4) We iterated our deck a LOT!

Storytelling is incredibly important for any fundraise. As a new VC, we had no brand and no product to show. In most cases, there’s literally *nothing* that differentiates a new VC from all the other fund managers.

The first version of our deck basically talked about how we had some edge because we went to “fancy” schools, worked at “fancy” jobs and were already active seed investors. And I remember my friend Tim Chae basically looking at that slide and saying that every fund manager on the fundraising circuit had everything we had. And he was right. The hundreds of new VCs who are out pitching right now all went to some permutation of fancy schools and/or worked at fancy companies and/or have done some fancy investing. These are not differentiators!

We quickly realized that we needed to be able to tell a differentiated story. For us, our biggest differentiator is around our model of how we invest – namely, we look heavily at speed of execution in investing the bulk of our fund. This was not only a story around being different but also around why our past experience has led us to this model and why we are uniquely qualified to invest in this way.

It took us about 20 versions of our slide deck to hit this story right. Thanks to so many people who gave us feedback on our story and especially to Tommy Leep, who helped us get our story on the right track early on. If you get the chance to work with him on your pitch – whether you’re a fund or a startup – do it.

5) We built momentum by packing in lots of meetings. I personally did 345 fundraising meetings between July 9, 2017 – May 25, 2018

In the past, I’ve written about how to generate fear of missing out (FOMO) amongst investors when you’re raising for your startup. In the beginning when you have raised nothing, it’s hard to generate FOMO. Whether raising money for a startup or a VC, no investor wants to be first check in. So the best way to show fundraising momentum when no money has been committed is to pack in a lot of fundraising meetings. This makes it easier to generate excitement when potential investors hear that other investors are doing second meetings with you. And you also want all investors to end up committing to you around the same time.

Once you get commits, then you can start talking with other potential investors about those commits, which generates even more commits. The key is that you need to constantly be meeting with people.

Here’s a graph of all my meetings per week between Summer 2017 and Spring of 2018:

Note: this doesn’t include all the meetings that my co-founder Eric Bahn did. We often did first meetings with potential investors individually. So collectively, our total number of meetings was much higher than 345!

You can also see from this graph that I began to run out of leads! This is the most important thing – don’t run out of leads! (more on that below)

6) We started with a low minimum check size to close investors quickly and raised it over time.

In the beginning, our minimum check size started at $25k and eventually it went all the way up to $300k (for individual investors). We did this to generate quick commits and create more FOMO.