I’ve written a little bit before about how venture capitalists (VCs) make money (see this post).

But I’ve never quite spelled it out, and in this post I’ll do just that. I think it’s useful to understand this — certainly for anyone who is an aspiring future VC — but even for entrepreneurs, because it helps to understand the mindset of people you’re pitching.

What is a Venture Capitalist (VC)?

At a high level, the concept of a VC is relatively straightforward — a VC is basically a middle (wo)man. On one side, a VC will raise money from rich people called Limited Partners (LPs). These can be individuals, families, corporations, and other funds who invest in funds, etc. VCs then take that money and on the other side, invest in startups. The hope is that some subset of those startups will grow tremendously, and then through some sort of liquidity event — it could be an acquisition or an IPO or even a way to sell shares to someone else in a secondary sale, the VC will receive back a lot more cash than initially invested. That cash then gets returned back to the initial investors and the VC makes some money in between.

Typical VC structure

A very common lifespan of a VC fund in the US is 10 years. In other countries, this varies quite a bit — in China, for example, VC funds have been set up to be closer to a 5 year time horizon.

The term is largely based on how long it will take to get liquidity on deals. Investors who invest in such a fund are committed to locking up their capital for 10 years. Now throughout the 10 years, it’s possible that investors may receive capital back from exits that happened before 10 years, but the bulk of the great exits will happen closer to the 10 year mark. For reference, Dropbox went IPO after 15 years, and so if you were an early stage investor, you would’ve made a lot of money, but that may not have happened for many years.

Side note: it is possible with the new Long Term Stock Exchange (LTSE) coming to fruition, we may see early stage VCs shorten their time horizons to getting liquidity. The bar to have a successful IPO on the NYSE and the NASDAQ has been raised considerably since the 90s, so companies have been staying private for much longer. If you look back at Amazon’s IPO in the 1990s, their valuation was pegged just over $400m. These days, Uber went public at over $80B valuation! If we enable more liquidity events at earlier stages, it’s possible we may see changes in fund lifespans.

In the US, a typical VC firm economics structure follows a 2% / 20% rule. The 2% rate represents management fees. And the 20% represents something called carry.

What are management fees?

Management fees are basically the operating budget for a VC firm on an annual basis. So in a 2% model, if you have a $10M fund, you have a $200,000 budget every year for the course of your fund.

If you have a $100m fund, with a 2% structure, you’d have an annual operating budget of $2 million each year. So as you can see, there is a stark difference in budget between a microfund and a large Sand Hill VC. And when people talk about VCs having nice salaries, they are referring to partners and employees who work at the latter type of firm — firms with a lot of money under management. Microfunds are very much like bootstrapped startups.

Let’s dive into the economics of a $10m fund. The $200,000 budget needs to cover just about everything. Certainly, it includes salaries, but it also needs to include other things like marketing expenses, health insurance and travel. If you have an office, that must fit under this budget too. And so if your typical microfund has two partners, they are definitely earning well under $100,000 per year, and more likely closer to $50,000 given that all expenses must fit under this $200,000 number. For us at Hustle Fund, in our 3 person partnership, we have publicly stated that we currently each make close to $50k per year and feel lucky to be able to bootstrap for a while.

What is carry?

The 20% represents the profit sharing of a VC fund. The way profits are distributed look something like this:

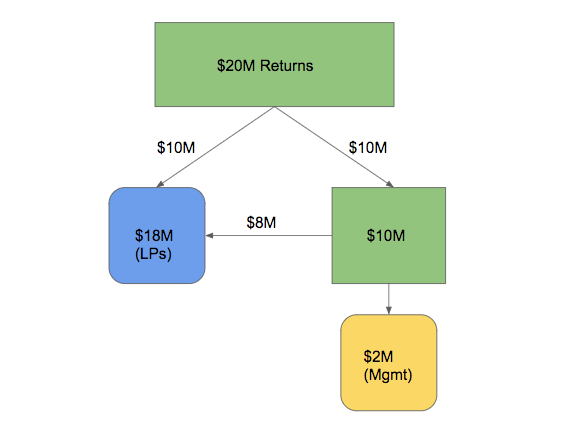

Say a $10m fund returns $20m. The initial $10m is first returned to the Limited Partners (LPs). Then the $10m profit is returned such that the fund managers receive 20% of this profit, or $2M (the yellow shape) in this example. That $2m is then distributed to the employees / partners of the fund based on however they’ve all mutually agreed to do so. (At Hustle Fund, all 3 partners have equal carry). And, the LPs receive the rest – $8M in this example, and so the LPs receive a total of $18m in this example (the blue shape).

Even though the fund returned 2x at a gross level, after all is distributed, LPs see a net multiple of 1.8x, because of the carry.

The power law of startups

Ok, now let’s look at the investing side. The interesting thing about the investing side is that startup outcomes are distributed very much in line with the power law. Namely, most startups will fail and will go to zero — i.e. you will lose your money entirely. Some will maybe return 2x or more. And if you have an excellent portfolio, you will capture a 100x-1000x returning company once in a while.

In order to succeed at investing in startups, you absolutely need at least one of these outliers in order to be successful. I hear all these non-investors or new investors talk about trying to find 3x multiples in startups. If you are investing at the early stages, you need to be aiming for much higher than that…

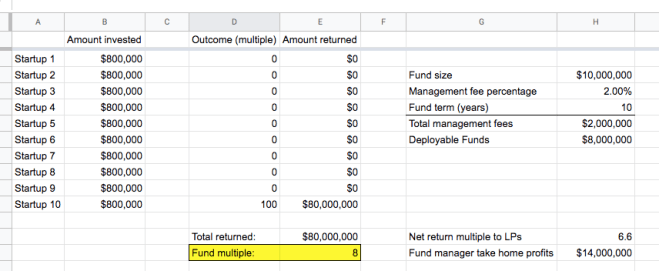

I put together this spreadsheet of startup outcomes that everyone can copy, so you can all play with the numbers.

Let’s look at the tab labeled “1 – 100x return”. If we assume the trite saying that 9/10 startups fail, and let’s say we have one big winner that delivers 100x returns, you can see that we can return an overall nice fund — 8x gross multiple, 6.6x net multiple to LPs. From this, you can see that it doesn’t matter that we have really low survivability in the portfolio. All that matters is that your one big winner was quite big.

Dilution impacts your returns as an early stage investor

Now, let’s add the impact of dilution back into this equation. Typically, a cap table will get diluted down by 10-30% each round, with an average being around 20%. Assuming that we are the earliest stage investors, this means that if a founder does 3 rounds of funding after ours, we will be diluted down by about 50%! So I modeled out the 100x winner as 50x in the next tab. You can see we are still returning good returns but if you aren’t aiming for 100x gross difference between your entry point and exit point in your investments, things start to get a bit dicey.

Can you improve survivability?

There’s a lot of debate amongst VCs about whether the 9/10 survivability that everyone touts is actually accurate. Can you help your companies survive longer so that you have more winners?

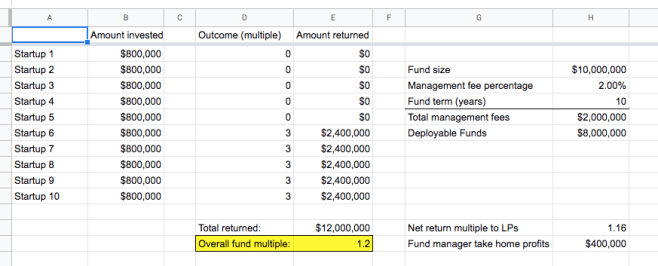

I personally think the answer is yes, but I think you still need at least one big winner to make the portfolio work out well. If we look at the tab labeled “5 – 3x returns”. You can see that even if we do phenomenally well with picking startups who have high survivability, if they are not returning much, our multiple on our fund is just barely over 1x and the net to LPs is basically that they get their money back. Wait, what is going on? There are a lot of 3x returners!

The primary reason for this is the management fees. Even though this VC fund isn’t making money off management fees — heck their budget is only $200k per year, on a $10m fund, $2m in total is used for management fees. In other words, this money isn’t being invested. So only $8m is invested, and so you have to overcome this initial hurdle to get to 1x. A lesser reason is once you cross the 1x hurdle, carry digs into some of the profits. (Side note: most VCs recycle small exits in order to invest more than 80% of their fund, but getting money back to recycle is not guaranteed and for the purpose of simplification, I removed that scenario.)

To be clear, this isn’t a situation that the managers of the fund want either. They are taking a puny salary of like $50k per year. And their profits are only $400k after 10 years of work that gets divided across the partnership — this is really dinky.

So you can play with the numbers on this spreadsheet, but you’ll find that even if you can increase survivability, you still need to be aiming for big winners.

How do you get a big winner?

Now, what does it mean to get a 100x returner? This means that if we invest at say $3m post money valuation, and the company sells for $300m, the difference in entry point and exit point is 100x. (Accounting for 3 rounds of dilution, this will be closer to a 50x returner).

Think about it — $300m is a big exit. It’s more than life-changing for most entrepreneurs. And many entrepreneurs might be tempted to sell even sooner. Heck $30m for most people is life changing. Remember, as a VC, we are the middle (wo)man, so we need that exit to be large for us to make a lot of money. But the entrepreneur doesn’t need a large exit to make good money. So there’s a bit of a disconnect there.

Large multiples occur when there’s a large spread between entry point valuation and exit valuation. VCs all have different strategies to achieve this. Some like to go in at low valuations and then sell for sub billion dollar exits. And this works, because there are many more exits that are sub $1B. And then there are VCs who have the exact opposite strategy. Entry point doesn’t matter, but they are gunning for an exit at a multi-billion dollar valuation. For example, Uber’s IPO was approximately at $80B valuation. If you got in at $5m valuation, then that’s on the order of a 10,000x multiple after accounting for dilution. So with that kind of exit, who cares if you got in at the $5m valuation or the $10m valuation or even higher — it’s all a wash at that scale.

But regardless of the strategy, all VCs aim to have large multiples.

You can also see that VCs can do VERY well if they end up getting a few 100x winners. Play with the spreadsheet — even with just one more 100x winner on the first spreadsheet, you can see that the net fund outcome to LPs goes up to 13x. So, a $100k investment into a fund turns into a million dollar outcome. On the flip side, more 3x outcomes on the last spreadsheet with near perfect survivability in a portfolio isn’t that awesome.

Takeaways

Based on all of this, this explains why VCs:

- May be valuation sensitive (depending on the strategy)

- Are only looking for super large outcomes and don’t care about good businesses

- Often pattern match — if they believe that “certain types of founders” can get funding easily, then they may have an easier time growing super large companies (I don’t believe in this personally, but this explains this behavior)

- Are looking for fast growth — winners must get to a billion dollar level within just a few years since a VC fund term is 10 years

- Fight over pro-rata — dilution can be rough so maintaining ownership in companies that are clearly strong winners is helpful to returns

- Don’t care about massive failures and would much prefer even just 1 “go big or go home” outcome to one that will be successful at a $50m outcome level.

I think following the money is always a good way to understand why people behave the way that they do. Hopefully these spreadsheets help to understand how VCs make their money.

Thank you for sharing this, Elizabeth. For the newcomers, like myself, wisdom from more experienced VCs like you is a gold mine.

LikeLike

thanks Aadil!

LikeLike

Learn something new every day. Thanks Liz! between you, my CFO and Brett Fox… I’ve learned so much relevant to relentless persistence in bringing a vision to life.

LikeLike

yet another infogold logical layout of a maze Thank you.

LikeLike

Very helpful to see it laid out like this. Thanks Elizabeth!

LikeLike

Elizabeth, is there a way to contact you via email, by any chance? I was humbly hoping to dicsuss a couple of topics, but I’m not sure replying to the subscription email was a good idea 🤔

LikeLike

Interesting read. Thanks. I love the transparency.

LikeLike

Now I get it! Thanks, Elizabeth for the information!

LikeLike